Aleksandr_Kravtsov/iStock via Getty Images

Aleksandr_Kravtsov/iStock via Getty Images

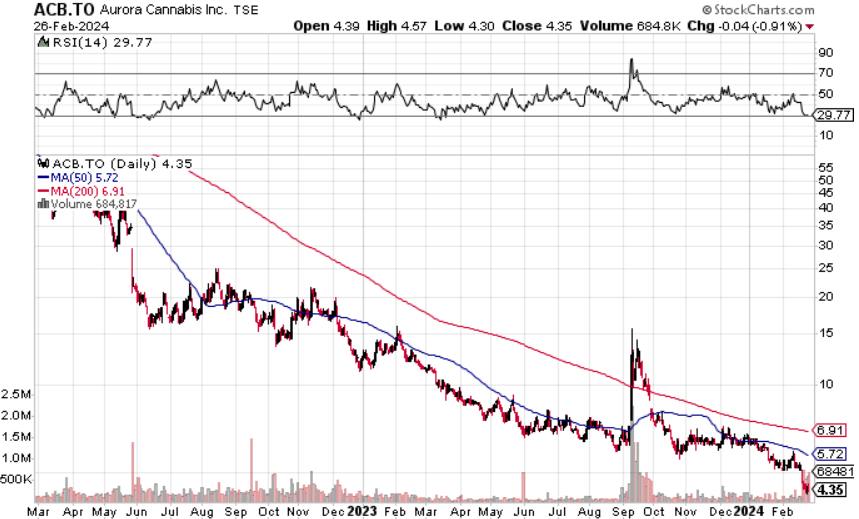

Aurora Cannabis (NASDAQ:ACB, ACB:CA) recently completed the consolidation of common shares on a 10:1 basis to maintain its minimum bid requirement to stay on the NASDAQ. This is the second time the company has done a reverse share split, with the first being back on May 11, 2020 on a 12:1 basis.

StockCharts

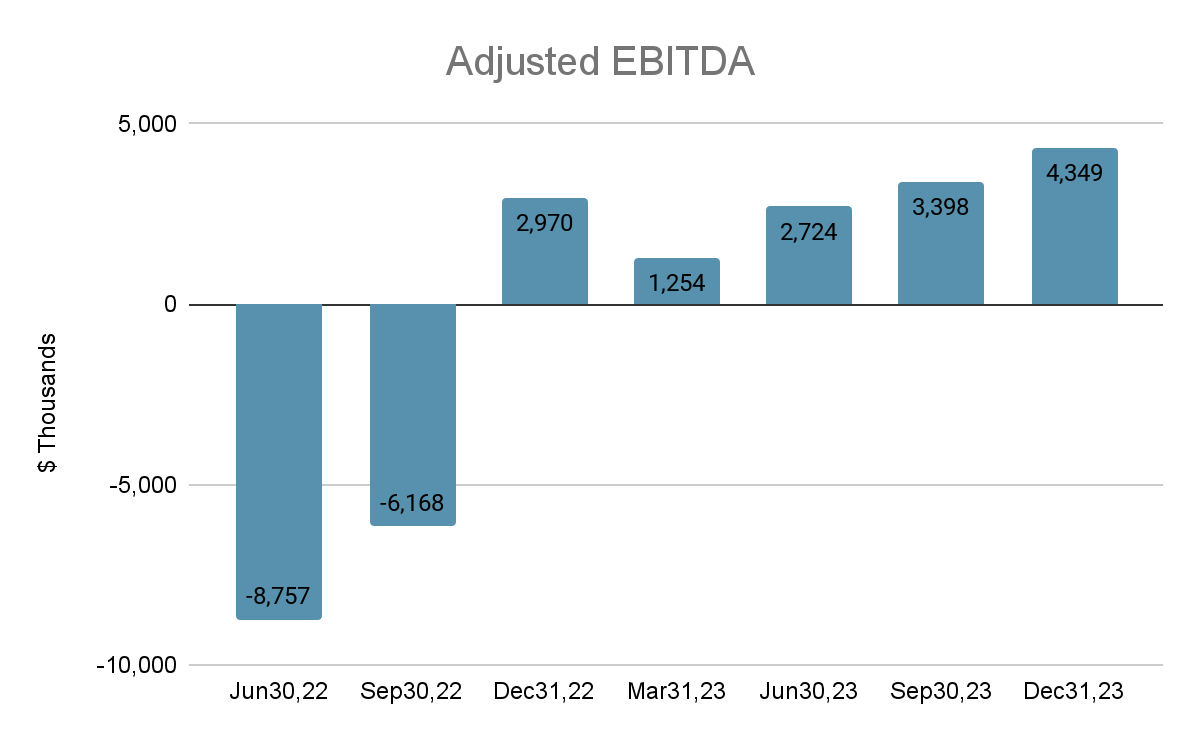

I previously suggested the company may turn around in 2023 and I may have been too early. But as absolutely bleak as the stock price chart looks there seem to be a number of significant positive developments not reflected in the price. For one, the company recently posted its fifth quarter of positive adjusted EBITDA (see chart below). Two, nearly CAD$540 of debt has been repaid over the past three years and the remaining will be settled in February 2024, leaving the company debt free. Finally, the company has provided guidance for achieving positive cash flow within this calendar year. After years of losses could such a financial milestone really manifest? In this article I explore this possibility and take a closer look at the two main drivers of top line growth.

Egon Zee Research, Aurora Cannabis

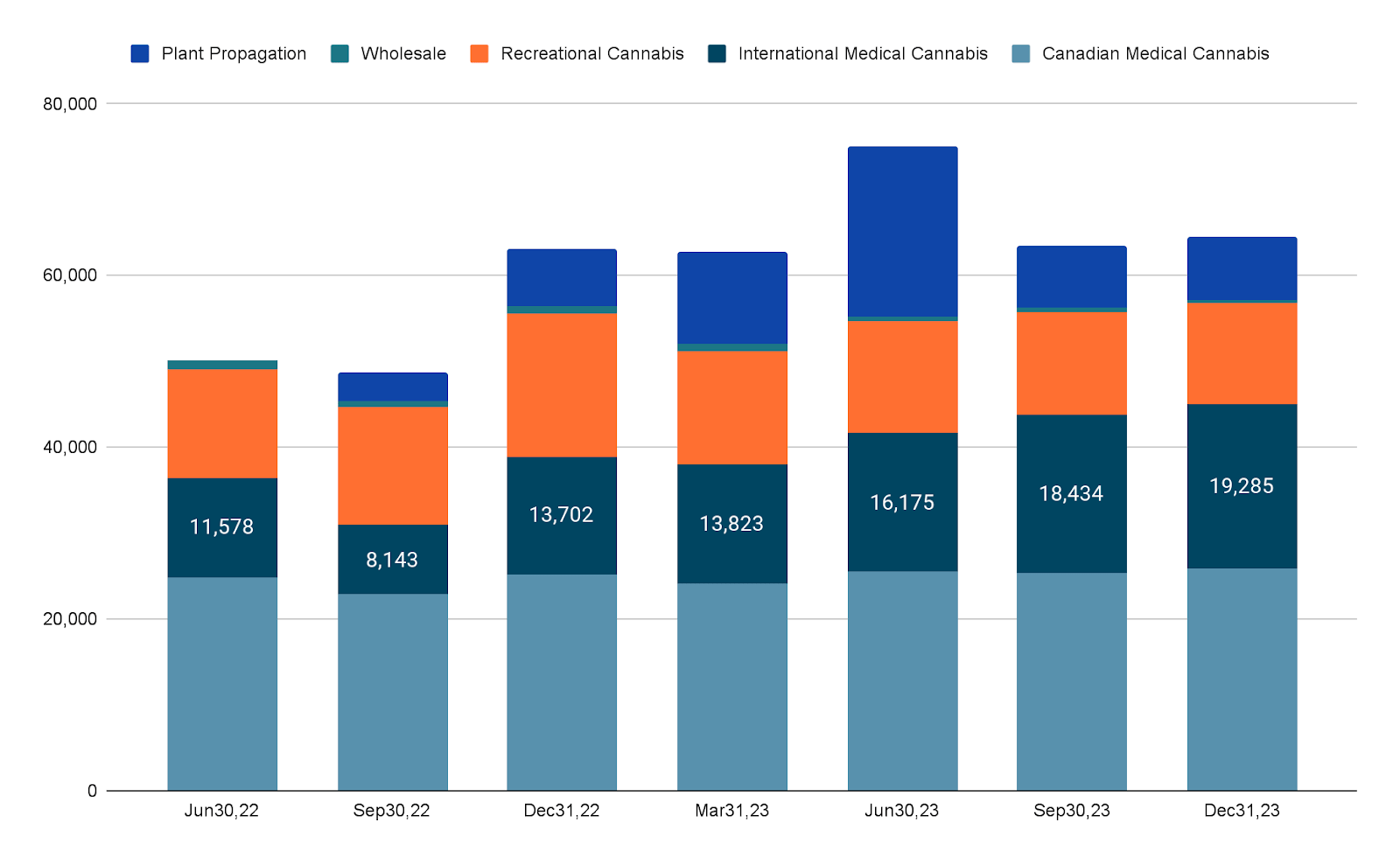

When Miguel Martin became CEO he brought a focus on the high-margin medical cannabis and shifted away from the crowded low-margin recreational business. In the short term this had meant quarter after quarter of decreasing revenue. Finally, though, we can see the strategy paying off as revenue has been growing year over year. Notably, the international medical business has had five quarters of increasing revenue (see chart below) and maintains margins in the low to mid 60%.

Egon Zee Research, Aurora Cannabis

On Feb. 7, 2024 the company announced it had bought out the remaining 90% interest in MedReleaf Australia to become the largest global medical cannabis company operating in nationally legal markets. The transaction is expected to be immediately accretive to adjusted EBITDA and deliver double-digit increases to profitability of the Australian business model, further accelerating the plan for positive free cash flow in 2024. In the last quarter ending Dec 31, 2023 the company recognized revenue of CAD$8.8 million for products sold to MedReleaf, which is roughly 46% of the international medical segment. As the transaction took place in February it will only partially contribute to this quarter's results and the full effect will be seen in the Apr-Jun quarter.

Other big news came as Germany approved a law to legalize recreational use of cannabis with strict rules and restrictions starting April 1. Medical companies and patients are said to be the biggest winners from this news as medical cannabis will no longer require a narcotic prescription form, simplifying the process for prescribing doctors and the supply chain. Aurora currently holds the #2 position in Germany and is one of only three companies with medical domestic production. Germany is the largest European market and Aurora's largest European share. This news may be the start of a domino effect that cascades across Europe. Note that the company already has a presence in seven European countries: Germany, Poland, UK, France, Switzerland, Malta, and the Czech Republic.

All in all, these two positive developments coming from Australia and Germany will begin materializing in the first half of this calendar year. By the end of year I wouldn't be surprised if the international medical segment actually surpasses the Canadian medical business.

Since taking a 50.1% controlling stake in Bevo Farms in Aug 2022 the company has been able to repurpose its idle or underutilized production assets (Aurora Sky and Aurora Sun). The first sales of orchids from the 800k sqft Aurora Sky facility should have already occurred last quarter and are said to represent a step function change in Bevo's revenue and EBITDA generation this calendar year as the orchid business hits steady state. Sales from the 1.6m sqft Aurora Sun should begin in the middle of this year. Through the use of these underutilized facilities the company even sees a potential path to doubling Bevo's revenue and cash flow over the next two to three years. Note that Bevo contributed around CAD$45.1mil over the past twelve months. Management will need to see a few months of sales before providing more guidance on this.

The plant propagation business has a seasonal cadence and delivers 2/3 of its annual revenue and adjusted EBITDA from January to June, with about 40-50% being delivered in the Apr-June quarter. That being said, this current quarter and the next should deliver quite a boost to Aurora's financials.

While the ship has certainly turned around there is still work to do as the company has diluted shareholders wildly over the past few years. I hope management addresses this issue in time.

The rate of adoption in Germany is still to be seen and could pick up much slower than anyone expects. The same can be said about legalization across other companies, so it is important not to get too carried away.

Even in the face of improving financials the market has had a very negative view on the cannabis industry for some time now so it may take sentiment longer than expected to shift the other way. Investors need to be extremely cautious and prudent with their investments in the sector.

As of writing Aurora has a market cap of CAD$237.25 million, a price-to-sales ratio of 0.63, and an RSI of 29 indicating it's oversold. The entire Canadian cannabis industry has taken a beating over the past few years but Aurora is setting itself apart from the group, showing tremendous improvement in its fundamentals. The company has reduced its costs significantly, is now debt free, and has proved itself by meeting its previous goal of positive adjusted EBITDA.

Finally, the company is guiding for positive cash flow this calendar year and not only do I think it'll meet that goal but I think that may occur as soon as the June ending quarter. I based this on the recent MedReleaf Australia buyout, cannabis legalization in Germany, and a step function increase in Bevo. Aurora seems inappropriately priced for bankruptcy, is grossly undervalued at this level, and I recommend it as a Strong Buy.