Win McNamee

Win McNamee

In my previous update in early January 2024, I urged investors in multi-family mREIT Arbor Realty Trust, Inc. (NYSE:ABR) to be cautious about adding more shares. While I admonished pessimistic ABR investors for being wrong in their prognostication in October 2023, I also exhorted bullish investors to wait for a more attractive entry point.

ABR has declined more than 10% (adjusted for dividends) since my January article, underperforming the S&P 500 (SPX) (SPY) significantly. Arbor Realty investors have also suffered the burden of short sellers bent on crashing the stock, as ABR's short interest as a percentage of its float has increased to more than 40% (as of late February 2024). Viceroy Research has been very vocal about its bearish thesis on ABR, with its initial short report in November 2023 calling ABR "the worst of the worst." The short seller contends that "its entire loan book is distressed and underlying collateral is vastly overstated." However, observant investors should recall that ABR surged from its November lows toward its December highs, easily dismantling Viceroy's bearish thesis.

Despite that, the short seller has remained steadfast about Arbor Realty, refuting ABR management's assurance at its fourth-quarter earnings. In addition, Viceroy also published another update on March 18 that "Arbor’s delinquencies are now well developed, as distressed loans flow from <30 days” to “>30 days." As a result, it's possible that ABR investors might have to anticipate a surge in delinquencies moving forward if Viceroy is correct about its report.

As a price action investor, I believe it's essential to remain objective about Arbor's challenges, as Viceroy is all but one participant in the marketplace. Price action allows us to pore through the buying/selling sentiments at different levels, indicating whether the market "agrees or disagrees" with Viceroy.

Moreover, even if Viceroy Research is correct about its report, it's also possible that the market would have reflected higher delinquencies over the next few quarters. Does it make sense, as the market is undeniably forward-looking? Recall that ABR fell toward its early February lows (pre-Q4 earnings) that nearly re-tested ABR's November 2023 lows but didn't. In other words, dip-buyers returned to support ABR in February, likely seeing significant valuation support at those levels, particularly for income-focused investors. Moreover, Arbor management has already indicated a "challenging environment and the potential for increased stress in the next couple of quarters" at its Q4 earnings conference. Therefore, I don't believe the market is dumb enough not to reflect these headwinds into ABR's price action and valuation.

ABR is valued at a forward dividend yield of 13.3%, well above its 10Y average of 9.6%. Its forward distributable earnings per share multiple of 7.7x is also well below its 10Y average of 10x. Therefore, the market is not foolish. Arbor management has communicated the challenges of defaults, also attributed to unhelpful behaviors among its borrowers. However, Arbor management highlighted that the company is confident it can resolve delinquencies expeditiously. In addition, its focus on multi-family housing remains intact. Arbor management also highlighted the significant losses in the office sector have not been experienced in Arbor's multi-family portfolio.

Furthermore, Arbor's FY23 performance has lifted investors' confidence that Arbor remains well-positioned to cover its dividend payout, with a payout ratio of about 70%. However, I believe the market has likely attempted to price in more significant challenges in 2024, likely attributed to a slower-than-expected FOMC rate cut cadence. Fed Chair Jerome Powell corroborated the FOMC's preference for three rate cuts in 2024, which aligns with the market's expectations. Hence, the lack of a negative surprise in the Fed's outlook should help bring more clarity to the market, as it tries to anticipate whether Arbor might be forced to cut its dividend per share markedly, in response to higher potential delinquencies.

Analysts' estimates have likely reflected these headwinds, with Arbor Realty's distributable EPS expected to decline 25% in 2024, threatening the sustainability of its dividends. However, with the Fed meeting the market's expectations, I believe ABR's medium-term bottoming in February seems increasingly robust. In other words, stronger-than-anticipated buying momentum could trigger a sharp short squeeze to squeeze out the short sellers still betting on the demise of ABR.

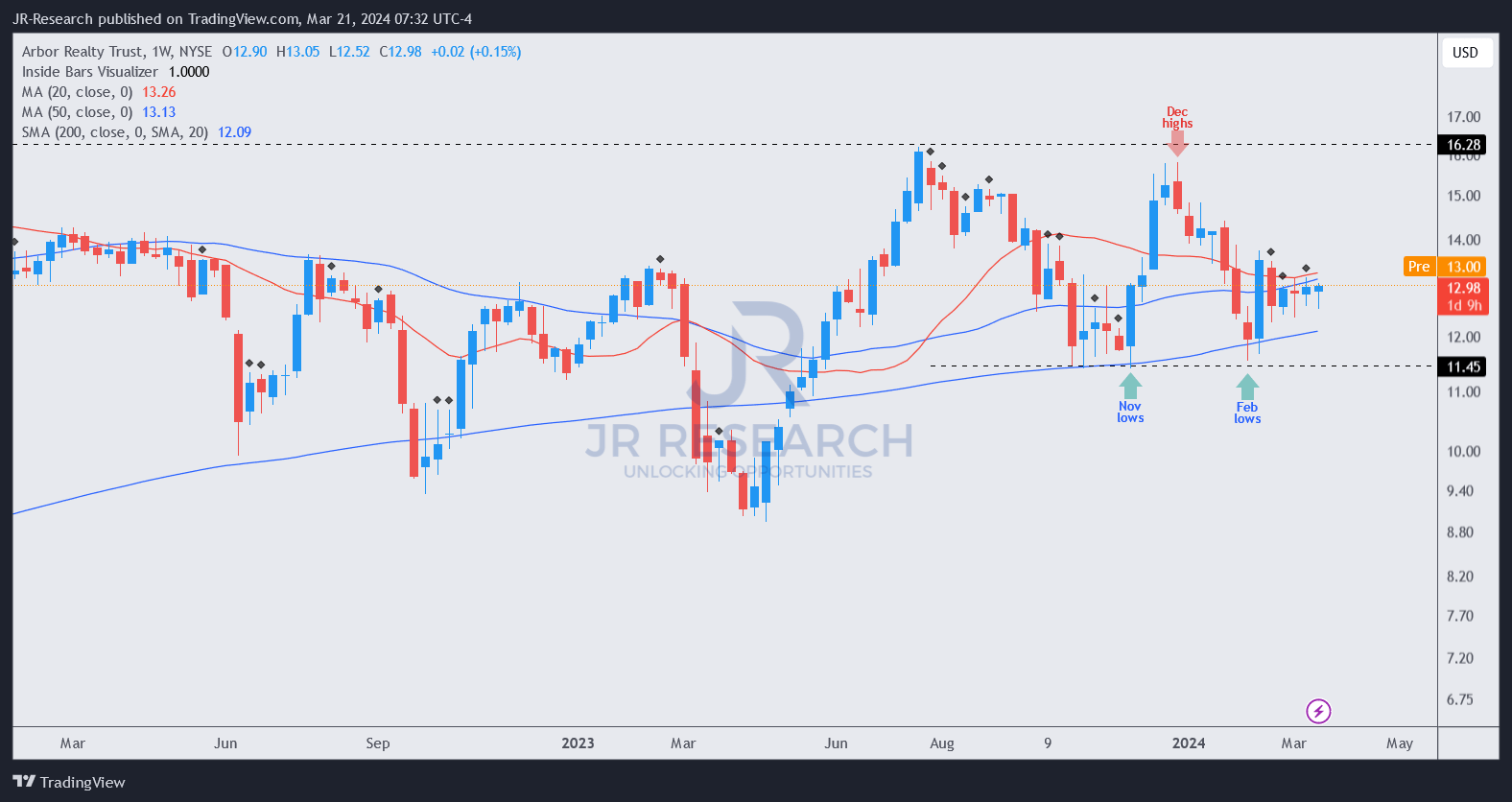

ABR price chart (weekly, medium-term, adjusted for dividends) (TradingView)

As seen above, ABR's February bottom at the $12 level remains robustly defended. It suggests that the market tried to price in these challenges as ABR fell significantly from its December 2023 highs (the market is forward-looking).

Notwithstanding the slew of updates as Viceroy Research tries to shape the bearish narrative, ABR buyers have remained relatively unperturbed at robust support levels. With the potential of a massive short squeeze brewing, as buyers continue to accumulate, I believe it's timely for ABR buyers to return and help squeeze out Viceroy for good.

Rating: Upgrade to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!