anurak phraisan/iStock via Getty Images

anurak phraisan/iStock via Getty Images

The Dividend Kings are stocks that have increased their dividends annually for 50+ years. It's a formidable list to enter. Only 47 stocks have made it. Consequently, it's a mark of distinction and points to long-term earnings and dividend safety.

In this article, I discuss three of my favorite Dividend Kings to buy for the long term. We analyze these stocks monthly using a previously described methodology. We typically emphasize earnings and dividend growth, dividend safety, and valuation. The three stocks are American States Water (AWR), Coca-Cola (KO), and ABM Industries (ABM), which are all long-term buys.

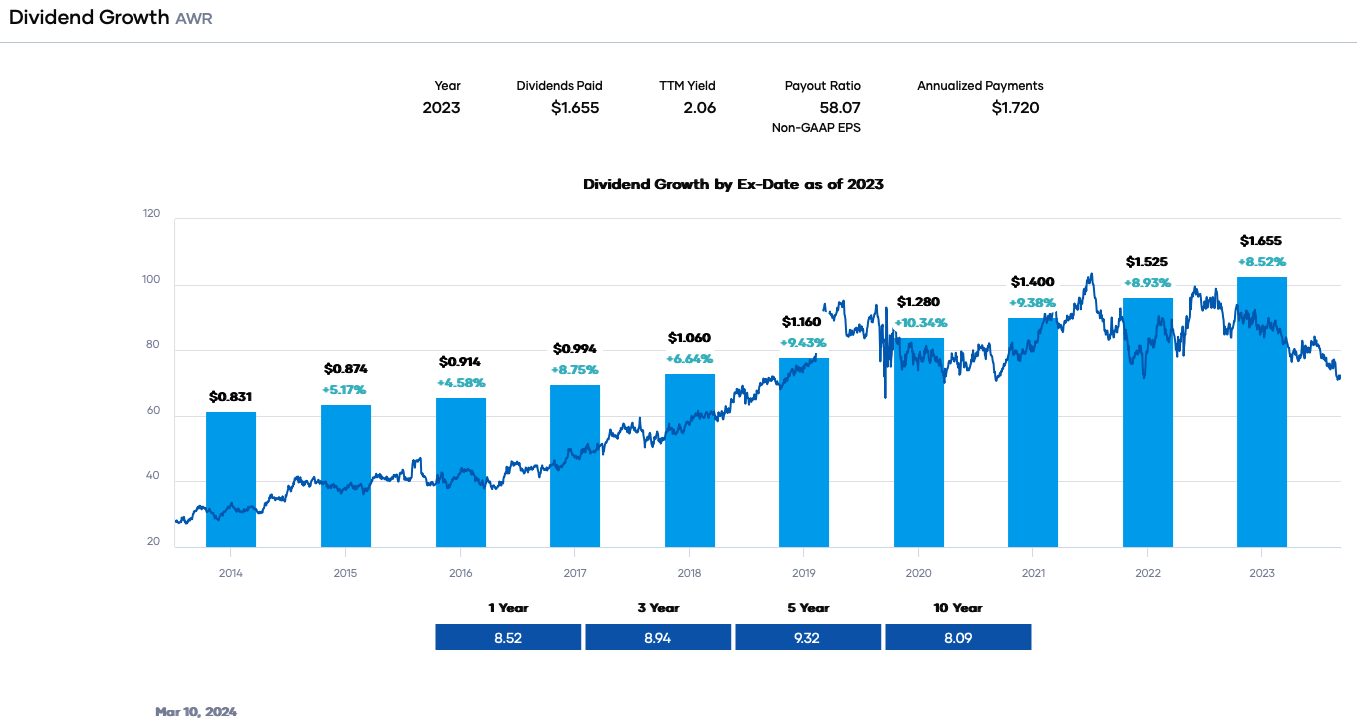

American States Water (AWR) is one of my favorite Dividend Kings. It is one of three water utilities on the list, meaning they are overrepresented because they are regulated monopolies providing essential services. Further, American States Water has the longest streak of increases of any equity, at 70 years.

The firm is a regulated water and electric utility operating primarily in California. It also has non-regulated water and wastewater contracts for 11 U.S. military bases. The regulated business consists of The Golden State Water Company, with around 264,100 water customers across ten counties, including the metropolitan Los Angeles area. This segment also has an electric utility business, Bear Valley Electric Service, with approximately 24,800 customers.

The company had revenue of ~$595.9 million in the last twelve months. It has a market capitalization of approximately $2.67 billion.

I like American States Water because its regulated business has effectively no competition and the long-term success in increasing its rate base. Revenue and earnings growth come from population increases and rate hikes. Water utilities invest in infrastructure to upgrade and maintain their treatment plants and water lines. Over the past several years, this activity has translated to about 9% compound annual growth rate (CAGR) of the rate base. As a result, earnings per share have climbed 10.6% on average in the past five years.

Adding to growth is the company’s non-regulated business. The company signs exceedingly long-dated contracts of 50 years with American military bases to provide water and wastewater services. This business gives American States Water predictable results for a third of its business on a very long-time horizon.

Despite its strengths, American States Water's share price has been under pressure, declining due to high-interest rates. As a result, the dividend yield has surged to ~2.4%. It sounds low but the yield is the highest since mid-2016. It is also well above the 5-year average of 1.7%.

The dividend has grown roughly 8% annually in the past decade, which is a high rate for utility. We expect future increases because of the firm's success in increasing rates and the reasonable payout ratio.

Portfolio Insight

The dividend safety is excellent, with an earnings payout ratio of 58%, generally low for a utility. Portfolio Insight’s dividend quality grade, a measure of earnings performance, revenue performance, dividend performance, profitability, and financial strength, is an ‘A+.’ This score means the equity is in the 95thpercentile of dividend-paying stocks. Lastly, the credit rating agencies give American States Water an A/A3, an upper-medium investment grade rating.

The utility is undervalued, trading at a price-to-earnings ratio of ~23.8X, well below the 5-year and 10-year ranges. It may not be dirt cheap, but it is a deal relative to historical averages. Additionally, despite consensus earnings expected to rise in 2024 and 2025, the stock price is near its 52-week low. I view American States Water as a long-term buy.

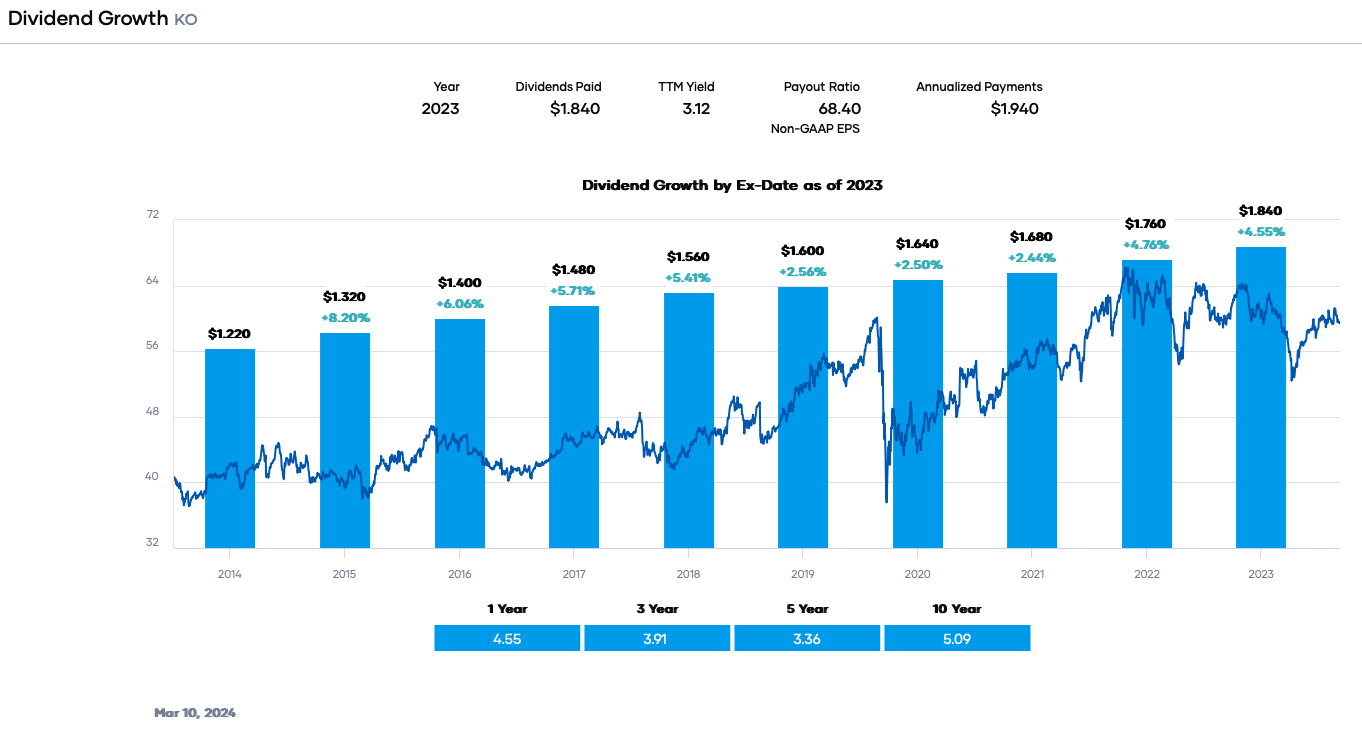

Next on our list is The Coca-Cola Company (KO), another favorite Dividend King. The beverage giant has a 62-year streak of increases. It most recently raised the dividend by about 5.4% in February 2024. Coca-Cola is a company that almost every investor knows. It is a dividend growth stock with one of the longest streaks of dividend payment. In addition, Warren Buffett's Berkshire Hathaway owns approximately 9.3%.

The firm was founded in 1886. Today, it is the largest non-alcoholic beverage company in the world, operating in more than 200 countries. It competes in essentially every category. The estimated market share is 46.3% in the United States, with five of the top 10 selling carbonated soft drinks. Twenty-six brands are billion-dollar ones, like Coke, Diet Coke, Sprite, Fanta, Dasani, Costa, etc. Total revenue was $45,754 million in 2023.

Coca-Cola's growth formula is simple. It adds to the top line organically and through M&A. Increasing volume, brand extensions, packaging innovation, and price hikes add to revenue and earnings. The firm also acts as an industry consolidator and periodically purchases smaller competitors. Its most recent acquisitions were BodyArmor and Costa Coffee. By buying new brands and leveraging Coca-Cola’s extensive distribution network, sales ramp up quickly.

The share price has remained flat in the past year despite strong organic growth and beating estimates. Investors seemingly favor Technology over Consumer Defensive stocks. However, the flat share price and rising dividends have caused the yield to reach nearly 3.3%, slightly above the 5-year average of 3.08%. The dividend has grown in the low single digits for the trailing five years. However, a declining payout ratio suggests the rate may pick up in the future.

Portfolio Insight

The yield is supported by a 68.4% payout ratio, which has fallen since the pandemic. Similarly, the free cash flow of $9,747 million exceeds the dividend payment of $7,952 million. The dividend safety is solid. Coca-Cola earns a 'B+' for the dividend quality grade, meaning it's in the 80th percentile. The credit ratings are A+/A1, an upper-medium investment grade rating. However, Coca-Cola’s dividend is probably safer than the above numbers suggest. It did not cut or suspend the dividend during the COVID-19 pandemic, a challenging time for the company.

Coca-Cola is undervalued because of rising earnings and a flat share price. It trades at a 21.2X forward earnings, below the 5-year and 10-year ranges. Moreover, consensus earnings are expected to be higher in 2024 and 2025. This, combined with the generous yield, long dividend payment history, and safety, makes this Dividend King attractive. I view it as a long-term buy.

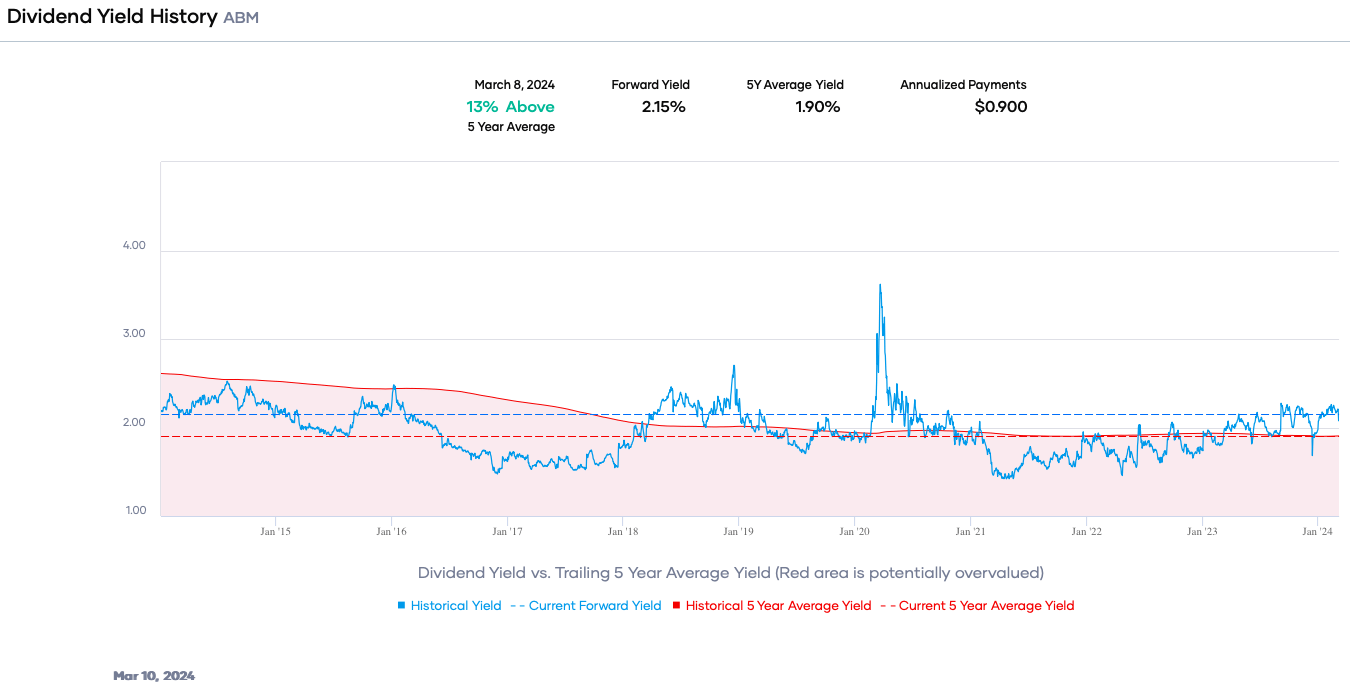

Our last pick is ABM Industries (ABM), which is probably one of the least well-known Dividend Kings. That said, it has a 57-year streak of dividend increases. Further, the 100+ year company provides essential services to clients, including janitorial, facilities, and parking services for commercial real estate, industrial, data center, distribution, schools, colleges, etc. It offers other services, too. Total revenue was $8,175 million in the last twelve months.

Competition is intense in these markets, and there is little barrier to entry. However, the company grows organically by adding clients or offering more services to existing ones. It also acquires competitors. In 2022, ABM Industries bought RavenVolt and Momentum Support, and in 2021, it purchased Able Services. The formula results in slow and steady top-line growth of about 4% to 6% annually.

That said, the share price has been relatively flat since mid-2021 because of the pandemic and weaker results in 2022 and 2023. Consequently, the dividend yield has risen to 2.15%, more than the 5-year average of 1.9%. The dividend growth rate is in the low-to-mid single digits. The modest payout ratio of around 25% indicates more increases to come. Free cash flow has fluctuated because of acquisitions and debt repayment, but it covers the $57 million required for the dividend. Furthermore, the ‘A’ credit rating adds to the dividend safety.

ABM Industries trades at a low P/E ratio of 12.3X. The stock is undervalued, and earnings are anticipated to increase in 2024 and 2025. ABM Industries is a long-term buy.

Portfolio Insight