Anton Dobrea

Anton Dobrea

Ambev (NYSE:ABEV) was essentially created by private equity group 3G in 2000 when it merged two Brazilian brewers; Brahma and Antarctic. The company went on to build a Latin American beer empire as it bought up brewers throughout Central and South America and now holds several monopoly-like positions in large markets, including over 60% volume share in countries including Brazil, Argentina, Peru, Bolivia, Uruguay, and El Salvador. Brazil is Ambev’s largest market, representing approximately half of the company’s business and is also home to its headquarters.

Ambev’s main business is clearly beer with brands such as Skol, Brahma, Antarctica, Quilmes, Labatt, Presidente and others. But the company also deals in soft drinks and non-alcoholic beverages with top brands such as Guaraná Antarctica and Fusion. Ambev also has a partnership with PepsiCo and currently owns the exclusive rights to bottle and distribute several Pepsi products in Brazil, including brands such as Pepsi, Gatorade, H2OH! and Lipton Iced Tea.

It's important to note that Ambev is majority owned by Anheuser-Busch InBev (BUD) (AB InBev), one of the world’s largest brewers. While Ambev and AB InBev are independent companies, the latter ultimately has control with approximately 62% of Ambev’s capital stock in its grasp. The relationship also means Ambev has licensing agreements to produce, bottle, sell and distribute several AB InBev products in Latin American countries, including brands such as Budweiser, Stella Artois, and Beck’s.

Ultimately, Ambev is a dominant brewer in Latin America with a strong and beneficial relationship with perhaps the most prominent global beer company.

Ambev's brands. (Ambev Annual and ESG Report 2022)

Source: Ambev Annual and ESG Report 2022

Scanning the return on invested capital (ROIC) of gigantic brewers such as AB InBev, Heineken (OTCQX:HEINY) and Carlsberg (CABGY), we see that they gravitate toward high single digit levels, perhaps symptomatic of a capital intensive and commodity-like business dependent largely on scale and destined to achieve returns modestly above the cost of capital. Many of the largest industry participants ultimately use significant leverage to increase returns on equity.

ROIC in the beer industry. (LSEG)

Source: LSEG

But Ambev seems to buck the trend in the brewing industry with ROIC settling closer to 20% through time. We attribute Ambev’s exceptional results to two main items. The first is Ambev’s huge market shares in key Latin American markets. It’s one thing to be a large global brewer, but scale in the brewing industry perhaps matters most on a regional level, and huge volume shares in several countries such as 81% in Argentina and 68% in Brazil (according to Morningstar) give Ambev truly dominant market positions. Such commanding market shares provide barriers to entry from scale, but they also mean Ambev has influential relationships with clients and market participants all through the production, distribution and sales channels. We also shouldn’t forget that beer distribution and brand marketing, in addition to production, are all scalable on a regional basis. Scale and experience in Latin America also help Ambev hedge volatile commodity costs and maintain pricing power which is a tough task for smaller competitors. Ambev’s market position is likely the main source of its sustained impressive level of returns.

The second item we often flag related to Ambev’s returns and profitability levels stems from its history of private equity influence and focus on cost control. Even through pandemic related headwinds, selling, general and administrative expenses were kept in check, and ROIC levels have already returned to approximately 20%. Tight cost control is engrained through programs such as zero-based budgeting which was implemented at the company well over a decade ago. The result is more reliable profitability levels.

An additional competitive advantage stemming from Ambev’s scale is its broad brand portfolio across all segments of the market. Such a brand portfolio is key considering how structural growth drivers such as brand premiumization can affect end markets. Ambev can essentially shift brand focus to ensure it captures its fair allocation of growth and can protect market share.

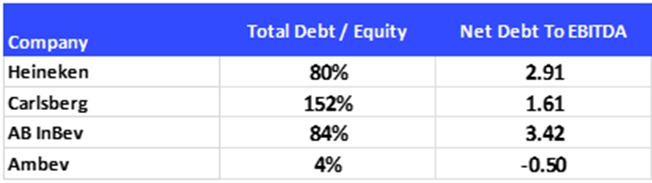

Ambev’s exceptional profitability likely contributes to another main difference from most competitors – its pristine balance sheet. The company has held a net cash position for well over a decade while other competitors have levered up in an apparent attempt to consolidate the industry and enhance returns. Ambev's competitors generally have much more leveraged balance sheets, with Debt or even Net Debt/EBITDA ratios generally close to 2x or above. We note that Ambev’s free cash flow conversion is helpful in this regard as it has been near or above 100% in recent years. Balance sheet strength brings a plethora of advantages including improved dividend safety and resilience during difficult times.

Ambev leverage versus peers. (LSEG)

Source: LSEG

Ambev gradually rolled-up the Latin American market through sizeable acquisitions, but its current monopoly-like positions and its relationship with AB InBev have made it more difficult to continue acquiring in recent years. Acquisitions have indeed slowed to a crawl, leaving ample cash for other capital allocation options.

Ambev acquisition net cash spend. (LSEG)

Source: LSEG

Remember that Ambev has a substantial net cash position so there is little need to use funds to pay down debt. The main destination for excess cash has ended up being dividends, partially due to the preferential tax treatment given to dividends in Brazil. Brazilian companies are permitted to distribute earnings to shareholders under the concept of an interest payment on shareholders’ equity. Amounts distributed by Ambev to its shareholders as interest on shareholders’ equity are deductible for purposes of income tax and social contributions. However, there are proposals to change the tax rules regarding these “dividends” paid as interest on shareholders’ equity which could impact Ambev’s dividend policy. But in the meantime, a dividend looks like the main avenue for capital allocation for the majority of free cash flow. We appreciate the dividend payments, but the advantaged tax treatment does perhaps restrict switching to stock buybacks when the share price is particularly depressed, as does the large shareholding by AB InBev. Overall, we rate Ambev’s capital allocation as effective, which would seem to agree with Morningstar’s Exemplary rating for capital allocation.

We haven’t written much about growth yet. It’s trickier than it may seem. Recent high inflation through the COVID pandemic years was passed through by way of pricing elevated nominal growth quite substantially in 2021 and 2022. Growth has now perhaps settled to something closer to an expected underlying industry growth rate in the low single-digits. Consensus estimates from LSEG as well as Morningstar projections point to a growth rate close to 5% in the coming years.

But growth in local Brazilian currency may not translate directly into growth in USD terms, as is painfully obvious in the figures below. Revenue in BRL essentially doubled over the last decade while it actually declined in USD. The culprit is the halving of the exchange rate over the same period.

Ambev growth in BRL and USD. (LSEG / Ambev Annual Reports)

Source: LSEG / Ambev Annual Reports

This clearly demonstrates what is perhaps the most substantial risk to the investment case – currency risk. Ambev is almost a pure play on Latin America, and its revenue is split among countries that have anything but stable currencies in relation to the USD (or our home currency the CHF). Unless investors are somehow able to hedge out the currency risk, there is no escaping its presence. Profitability is less of an issue than growth as Ambev hedges most of its costs over about a year period and has strong pricing power, but the risk to foreign investors remains, nonetheless.

Latin America as a region has considerable macroeconomic and political risks, including potential changes to tax regulation in Brazil. Oddly, Ambev also has indirect exposure to commodities as beer volume is correlated with GDP per capita in Ambev's markets while GDP itself is correlated with commodity prices in a region rich in basic materials.

There is also some risk that health and wellness trends will lead to lower alcohol consumption over time, but Ambev’s non-alcoholic offering provides some hedge against the possibility.

Ultimately, Ambev’s strong market position in the Latin American beer market and its ability to churn out attractive return on investment and impressive dividends make it an attractive investment candidate from our view, even if growth prospects are more modest. Of course, investors must be willing to take on the substantial currency, commodity and political risks.

If the risks are deemed acceptable, valuation is the next focus. Ambev historically produced gross margins in the range of 65% with net margins even occasionally popping above 30%. But the COVID pandemic and its associated inflation changed all of that, at least temporarily. Beer volume flowing through channels like restaurants and public events was obviously affected as erratic ordering and inventory patterns even created periods of inventory glut, sometimes resulting in a promotional market back-drop. Ambev did push through substantial price increases, but matching prices with cost inflation and production with inventory through the past few years has been an exceptional challenge. Hedging also became more expensive. Gross margins dropped to approximately 50% with the net margin now approximately 18%. Modeling margins for the coming years is a difficult endeavor. Will they recover to historic averages or stay at depressed pandemic-levels? Maybe something in between?

We put together a discounted cash flow valuation model in USD to assess downside risk and the possibility that the current share price is an attractive entry point. The following are the key inputs used in our model:

Our model sticks the fair value close to $3.00 per share for the ADR listed in the US which is our preferred way to invest in Ambev. We view the model as relatively conservative since it bakes in little margin recovery to historic levels, so we conclude that downside risk in a base case scenario is perhaps limited with the share trading near $2.50. The share price might even offer an attractive entry point for investors willing to accept a modest margin of safety or with a more bullish outlook.

We do see a possible bullish path that would tilt the skew of risk firmly to the upside. For example, if we model gross margins recovering to 61% (the long-term average), the fair value moves nicely above $4.00 per share, offering material upside. One could conclude that there is substantially more upside than downside risk, which is something we look for when researching companies. However, it is possible that Ambev’s profitability and return on investment trend down to levels more in-line with its large global peers, which would likely have a negative impact on the share price.

Speaking more speculatively, it’s possible that AB InBev will look to consolidate the remainder of Ambev that it does not own if it can’t find other material M&A options following its acquisition of SABMiller.

We might also note that First Eagle, an investor we respect, owns a substantial position in the Ambev ADR. In an interview from late January of 2024 on Wealthtrack, Matthew McLennan from First Eagle responds to Consuelo Mack’s question about finding high-quality companies selling at discounts as follows.

“You can imagine in an environment like 2023, when people really wanted to jump on the growth train in the United States, that perhaps the value was outside of the United States in areas that had more apparent mundanity. And to give you an example of that, there's a company that we own. In fact, it's our largest investment in Brazil called Ambev, and this is the leading brewer, beer maker in Latin America. In fact, they have over two-thirds of the market for 80% of their operating income. So they have businesses not just in Brazil but throughout, all throughout Latin America and the Caribbean and even in Canada. Very strong market share position. Some of their core brands have been around for over a century. And the business is growing and, you know, you have no debt, you have net cash, you have a 6% dividend yield. And, you know, a valuation is very sensible. And so if you're willing to buy something that's seen as a little more stodgy in this environment, then I think something like an Ambev, because of its emerging market taint, if you will, is quite reasonably valued.”

We conclude that Ambev’s dominant positions in various Latin American beer markets represent a resilient business in the Consumer Staples industry. Combined with a strong balance sheet and attractive dividend, Ambev ticks several key boxes for investors interested in a high-quality investment option outside the U.S. market. But investors must be wary of the substantial currency risk which may also continue to dampen growth in USD terms as it has over the past decade. Latin American economies are also linked with commodity risk as well as a multitude of political and macroeconomic risks, including proposed changes to Brazilian tax regulation. However, we feel that the risks to Ambev’s investment case are, to a substantial degree, baked into the current share price, resulting in a reasonable valuation that perhaps offers skew to the upside in terms of possible outcomes. We hope to add the high-quality and resilient profile that Ambev offers to our portfolio, and we hope to do it soon.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.