pixelfit

pixelfit

AllianceBernstein Holding L.P. (NYSE:AB) looks like a compelling case for an investment. The company is expected to grow revenue and earnings at a strong pace in 2024 according to consensus estimates. The company's low valuation leaves plenty of room to the upside for the stock. AB looks more attractive than its peers on a valuation basis. As a result, the stock has a reasonable chance of outperforming its peers in 2024. Plus, AB pays a high dividend of nearly 8%.

AllianceBernstein is currently a global $3.9 billion market cap company that operates as a publicly-owned investment manager. The company manages individual client portfolios consisting of a variety of instruments such as: securities, currencies, private equity, commodities, fixed-income investments, and real-estate related investments. AB uses various strategies such as: long-term buys, short-term trading, short selling, options strategies, and margin transactions as its investments.

AllianceBernstein reports revenue among the following segments: Institutions, Retail, Private Wealth Management, Bernstein Research Services, and Other. The Institutions segment comprises 16% of total revenue and handles asset management for private/public pension plans, governments, central banks, insurance companies, and foundations/endowments. Retail is the largest segment, which comprises 45% of total revenue. The Retail segment handles investment management to individual retail investors.

Private Wealth Management comprises 25% and offers wealth management to high-net worth individuals and families. Bernstein Research Services comprises 9% of total revenue and offers fundamental & quantitative research & trade execution services to institutional clients. The company also has an 'Other' segment which comprises the remaining 5%. However, I couldn't find an explanation from AB on what type of business is included in the 'Other' segment.

AB looks set to benefit from the expected industry tailwinds over the next several years. The global wealth management market is expected to grow at a strong pace of about 10.7% annually to 2030. This would take the market value from about $1.7 trillion in 2023 to an impressive $3.4 trillion by 2030. This strong expected growth is attributed to growing demand for alternative investments such as commodities, private equity, real estate investment trusts [REITs], etc.

One of the growing trends that could pose a long-term threat to AB's business is the robo advisory segment which is growing at 26.4% annually. Robo Advisory involves the use of technology such as software, apps, and even AI to help individuals and groups to growth wealth. However, the good news for AB is that the traditional human advisory business model is expected to maintain a leading position through 2030. This gives AB the chance to consider developing a robo-advisory solution to remain competitive in the future.

AB is set to benefit from the industry growth since the company offers these alternative investments to clients along with traditional ones. The company sees a lot of opportunity to grow as U.S. money market funds reached a record of $6 trillion at the beginning of 2024. AB believes that some of money will find its way into investments with higher returns as the interest rate cycle shifts later this year in the form of rate cuts.

AB also has key strategies to help grow its business segments to benefit from the industry growth tailwinds. The company launched 10 active ETFs in Q4 2024, bringing AB's total to 12 ETFs with $1.5 billion in assets under management [AUM]. AB has ETFs that consist of equities and others that consist of fixed income investments. These ETFs can help generate more revenue for AB as they address investors' specific goals. For example, AB has a high dividend ETF that can help investors who have income and capital appreciation as investing goals. Another example is AB's Low Volatility Equity ETF which can attract investors who strive to outperform the market with less price volatility.

Another strategy for AllianceBernstein is growing its relationship with Equitable Holdings (EQH) to support AB's private markets platform. AB is 64% owned by Equitable. AB's private markets platform grew to $61 billion after a 9% year-over-year gain in Q4 2023 over Q4 2022. AB has a goal to grow this to $90 billion to $100 billion by 2027. This effort can be supported by Equitable's $20 billion capital commitment. By reaching that goal, private markets would comprise over 20% of AB's asset management revenue.

AllianceBernstein is valued attractively below its Asset Management peers. AB is trading at only 10.8x expected EPS of $3.01 for 2024. Cohen & Steers (CNS) is trading higher at 23.4x expected EPS of $3.12 for 2024. Artisan Partners Asset Management (APAM) is also trading higher than AB at 13.5x expected EPS of $3.24 for 2024.

APAM has the highest expected earnings growth for 2024 according to consensus at 12%. However, AllianceBernstein is very close with 11.7% expected earnings growth. CNS lags a bit with 9.7% expected earnings growth. AllianceBernstein looks to be the most attractive investment in my opinion with a significantly lower PE and with strong earnings growth. The low PE ratio gives AB more room to move higher as earnings growth catalyzes the stock.

The reason for AB's low valuation was a result of the stock's poor performance over the past year. The stock declined 18% over the past 12 months. The decrease was likely the result of the company's revenue and earnings miss for Q2 2023. AB missed revenue estimates by 2.5% or $20.78 million and missed EPS estimates by 7.6% or $0.05. This led the stock to sell off about 21% from about $33 at the time of the earnings report down to $26 by November 2023.

AB performed better in Q3 and Q4 of 2023 as estimates were exceeded for revenue and earnings. I think this trend can continue as AB employs its strategies as discussed in the Growth section of the article. The company's strategies are likely to allow AB to capitalize on the expected industry growth.

AllianceBernstein has an attractive dividend yield of 8%. AB's dividend yield exceeds its peers. Cohen & Steers pays a 3% dividend while APAM pays a 6% dividend.

It is important to note that AB has a 100% payout ratio. AB pays all of its operating cash flow out as dividends. This means that the company would have to either issue new stock or issue new debt to pay for an acquisition or for share buybacks. With a 100% payout ratio, shareholders get the full benefit from AB's operating cash flow. AB tends to prefer issuing new stock which they have done in past years. The company carries zero debt. So, we can reasonably expect new stock to be issued as needed. The downside to that is more shares can dilute shareholders which could suppress the price of the stock.

Another downside to the 100% payout ratio is the annual dividend raises are only as good as AB's operating cash flow growth. For example, AB's operating cash flow declined 19% from 2022 to 2023. As a result, the amount paid in dividends declined by approximately the same amount. The good news is that AB's expected earnings growth of 12% for 2024 is likely to lead to a gain in operating cash flow. So, investors may see increased dividend payments this year.

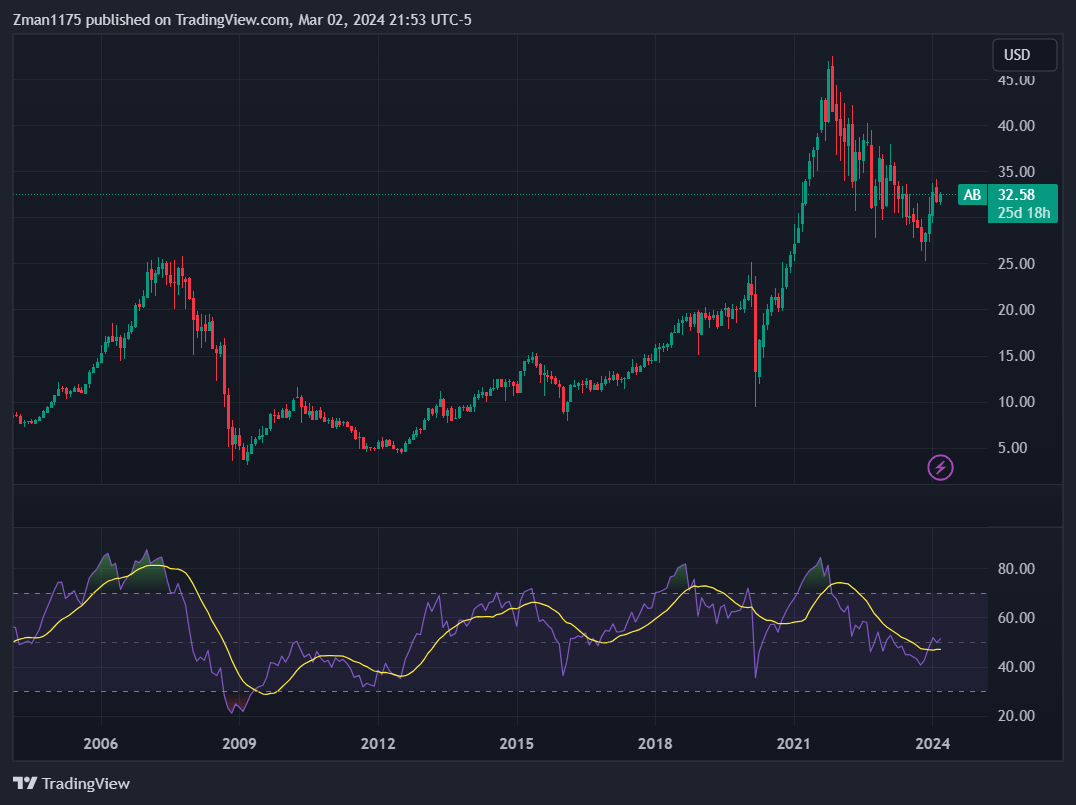

AllianceBernstein (AB) Monthly Chart with RSI (Tradingview)

AB's monthly chart above shows the stock in a large long-term bull flag formation from 2020 to the present. It looks like the stock is about to break higher in 2024 as the purple RSI indicator at the bottom of the chart recently increased above its moving average and above the 50 line. This shows positive upward momentum. The positive momentum has a good chance to continue in 2024 as the company grows earnings from the low, attractive valuation level.

The company appears to have solid strategies in place to benefit from the expected industry growth through the remainder of the decade. The launch of multiple ETFs can help AB grow revenue from fees. Growing the private markets platform should also help drive long-term revenue growth over multiple years.

Analysts have a one-year price target of $39 for the stock, which is about 20% higher than the current price. This target can be easily achieved from the company's expected earnings growth of 12% for 2024 with a multiple expansion boost from AB's low PE of 10.8. The price target of $39 would take the PE to about 13 based on expected EPS of $3.01 for 2024. That's still below the PE of AB's peers, CNS and APAM.