kynny/iStock via Getty Images

kynny/iStock via Getty Images

By Robert Carnell, Regional Head of Research, Asia-Pacific

Most Asian economies are very open to trade, and so a global slowdown ought to be bad news. Since Mainland China is typically the single biggest trade partner for Asian economies (India being an exception, which is one of the reasons why it outperformed the region as a whole in 2023), this ought to add a further dampener to export and consequently growth outlooks.

The reality of the situation though is that after a very weak 2022 and 2023, the export figures are beginning to turn higher.

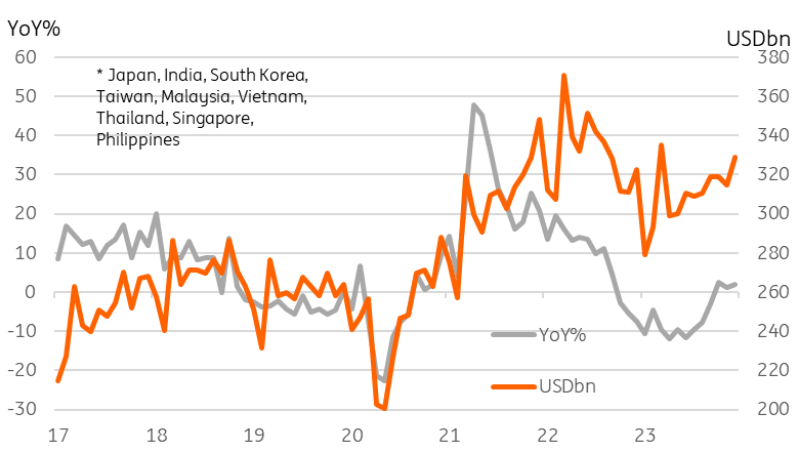

In the chart that follows, we show aggregate exports for non-China Asia in terms of the year-on-year growth rate. But because there has been so much volatility in recent years which can dominate such growth figures, we also show this in USD terms, which helps to put the numbers into a better perspective.

The year-on-year figures have improved and are hovering around zero after registering declines in all of 2023. But as the USD series shows, there has been some solid improvement. The trough in exports has evidently now passed, and while this looks more like a grind higher rather than a solid bounce, the direction is helpful.

Asian exports

Broken down by major export end destinations, it shows that imports to both the US and China are doing better. The same cannot be said for Europe. And this broadly fits our picture of the health of the rest of the world (see our other notes).

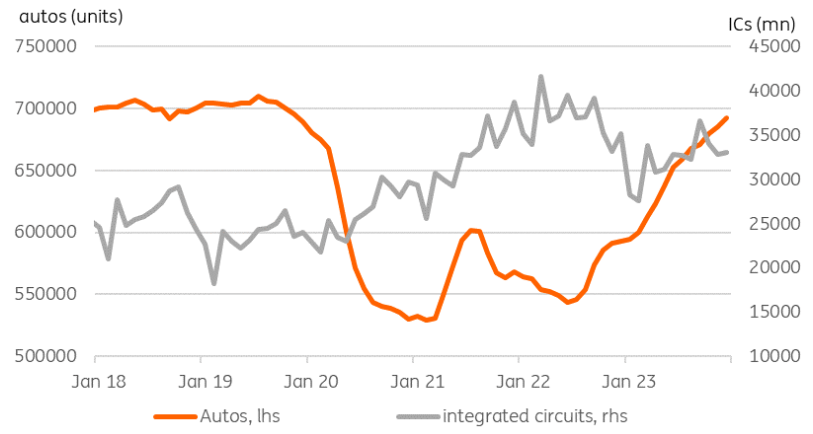

Underlying this improvement in the export performance for much of the region are two particular sectors which seem to be outperforming. The first of these is the semiconductor industry. This is particularly clear at the high end of the market and less pronounced for what we might term 'legacy' chips. As a result, the export growth rates for both South Korea and Taiwan are running much stronger than for the region as a whole, with Japan also seeing some outperformance. Notwithstanding the particular health of the industry leaders in this sector, a return to positive semiconductor demand should bode well for both exports and production figures across most of the region.

The other sector that is helping this regional improvement is autos. Whether this is still a pent-up replacement cycle following the pandemic or a feature of the growing demand for electric vehicles is not clear. It is also possible that this is also providing some support for the semiconductor industry, considering how full modern cars are of semiconductors these days. Again, South Korea and Japan benefit particularly from this, but so do other auto manufacturing sites such as Thailand.

Exports of autos* and integrated circuits**

This export recovery is not without any risks, though. The Red Sea conflict is causing the shipping costs for the region to rise significantly. The Financial Times recently published an article about why it's OK to be complacent about the Red Sea conflict. We don’t agree. At least not for Asia. The costs for re-routing container ships from Asia around the Cape of Good Hope rather than taking the shorter route through the Red Sea will add 10-14 days to the transit time of ships from Asia to Europe. And this is estimated to cost the shipping lines 20-25% more. For those wishing to charter a container from Shanghai to Rotterdam, the cost has risen three to four times from its 2023 lows. Other sea routes are also showing much higher container day rates as ships stay at sea longer and their availability diminishes. This may make some exports unprofitable and squeeze the margins of others, as well as likely pushing up the end costs for importers and consumers in the destination countries.

Moreover, this is still very early days. The increase may currently look small compared to the supply chain disruptions of the pandemic, but this is not to say that the current situation is where it ends. It may be, in which case the situation is likely to be manageable. But the situation is extremely fluid, so taking the current backdrop as an accurate indication of where this ends up seems ill-conceived.

One final positive feature of the region is the much more benign inflation backdrop. There is perhaps no better example of this in the Asia-Pacific region than Australia, where consumer price inflation has fallen from a high of 8.4% in December last year, to just 3.4% in December 2023. This is just 0.4 percentage points above the top of the Reserve Bank of Australia’s target rate for inflation. This certainly helps the growth outlook as real wage growth is now improving again. And where available, we can see the positive impact of this in an upturn in service sector PMIs.

That said, base effects have been doing a lot of the work in bringing inflation rates down. And we may well see some upward drift again in inflation over the first half of 2024, which is likely to prevent any of the central banks in the region from moving ahead of any potential Fed cuts.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.