Dilok Klaisataporn

Dilok Klaisataporn

The Direxion Daily Technology Bull 3X Shares ETF (NYSEARCA:TECL) is a leveraged ETF designed to provide three times the daily investment results, before fees and expenses, of the Technology Select Sector Index (IXTTR). Launched on December 17, 2008, TECL seeks to magnify the returns of the technology sector, which encompasses industries such as software, semiconductors, IT services, and telecommunications equipment, among others.

Despite its allure for potentially magnified gains, investors (and traders) should proceed with caution. Leveraged ETFs, by their nature, are primarily suited for short-term investment strategies, not least because of the compounding effect of their daily returns.

At present, amidst an uncertain investment environment, and notably high valuations of key index constituents like Microsoft Corporation (MSFT) and Apple Inc. (AAPL), we are maintaining a Sell recommendation on TECL.

Leveraged ETFs, like TECL, aim to deliver multiples of the daily performance of the indices they track. They enable investors to gain amplified exposure to the underlying index's performance using financial instruments like swaps and futures contracts. Specifically, TECL aims to provide 300% of the daily performance of the Technology Select Sector Index, making it a potent tool for experienced investors seeking to capitalize on short-term movements in the technology sector.

TECL achieves its leverage through the use of equity swaps, which are derivative contracts where two parties exchange streams of cash flows based on the performance of a stock or an equity index. These swaps allow TECL to gain exposure to the technology sector's performance without directly holding the stocks, providing a mechanism to achieve the desired leverage while managing risk and investment exposure efficiently.

To be clear, the fund will also own the individual securities in the index, and use swaps to magnify its exposure to the index and its constituents to magnify its exposure in order to generate the fund's target 3x daily return of the index.

Leveraged ETFs, including TECL, are primarily designed for short-term trading strategies due to the compounding effects of their daily returns, especially in volatile markets. Their structure and investment objectives mean they are not suited for long-term holds as the impact of daily rebalancing can lead to performance divergence over time from the underlying index, particularly in fluctuating market conditions. As the fund's summary prospectus states:

"The return for investors that invest for periods longer or shorter than a trading day should not be expected to be 300% of the performance of the Index for the period. The return of the Fund for a period longer than a trading day will be the result of each trading day's compounded return over the period, which will very likely differ from 300% of the return of the Index for that period."

The Direxion Daily Technology Bull 3X Shares ETF (TECL) tracks the Technology Select Sector Index, which has significant exposure to major tech companies.

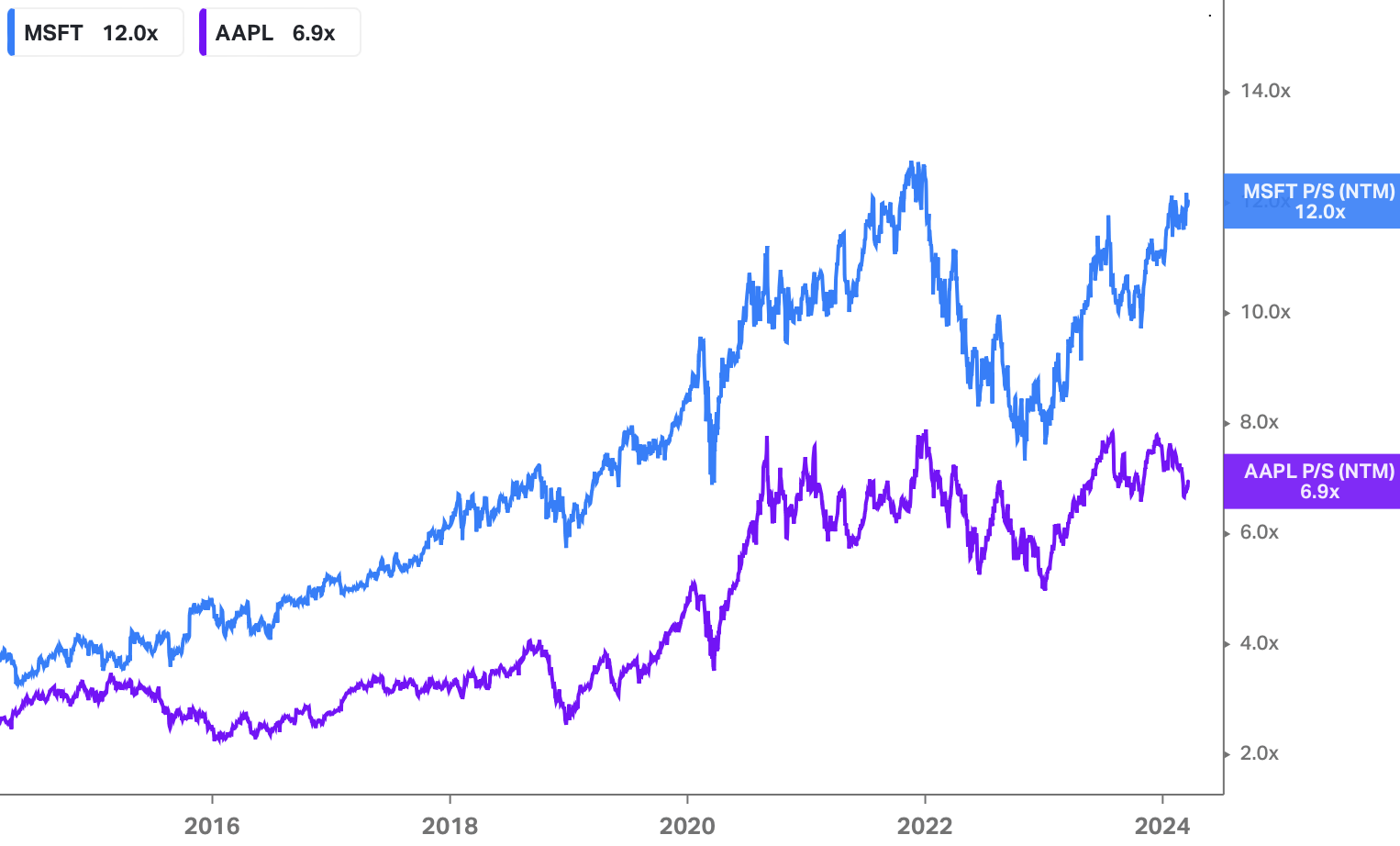

Microsoft Corporation (MSFT) and Apple Inc. (AAPL), which collectively made up over 40% of the index as of 12/31/23, are currently trading near their 10-year highs on a next-twelve-months price-to-sales (NTM P/S) basis at 12.0x and 6.9x, respectively, as shown in the chart below.

MSFT & AAPL: Historical NTM P/S (Koyfin)

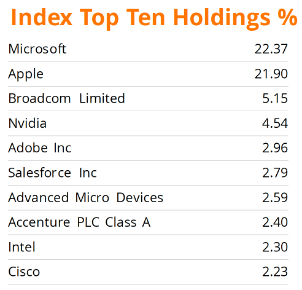

As shown in the table below, the index (and thus the fund) also holds positions, albeit much smaller ones, in other optically expensive tech companies like NVIDIA Corporation (NVDA) and Broadcom Inc. (AVGO) which currently trade at NTM P/S multiples of 19.8x and 10.9x, respectively.

Technology Select Sector Index - Top 10 Holdings (Direxion)

For comparison, broader market ETFs like QQQ and IVV trade at much lower NTM P/S ratios of 4.6x and 2.7x, respectively, underscoring the premium valuation of the tech giants in TECL as well as the impact of TECL's high concentration in a select few optically expensive stocks (in our view).

Remember, by investing in TECL your exposure is essentially 3x that of the underlying index. We recognize that the weightings of the constituents in the index, and thus TECL's holdings, are subject to change. However, with ~40% of the index concentrated in just two stocks that look historically expensive to us, we think even a short-term position in TECL could expose investors to significant downside risk.

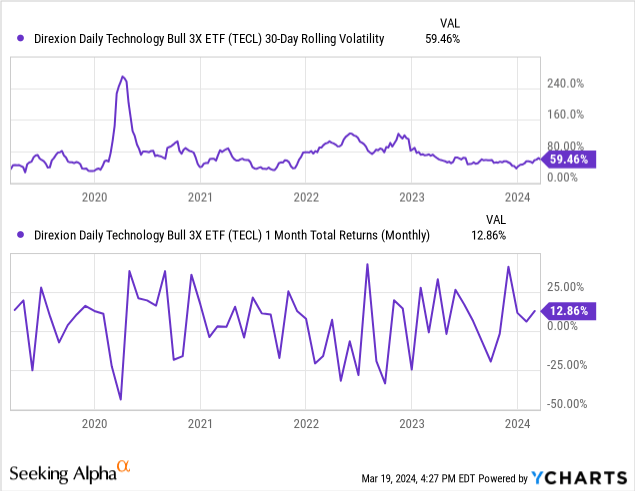

Since TECL is a short-term investment vehicle, we think it's more useful to review the performance of the fund over short-term intervals, in an effort to highlight the volatility of returns investors in TECL could experience even during relatively short hold periods. The charts below show the rolling 30-day volatility and rolling one-month returns for TECL over the last five years.

As these charts show, TECL is highly volatile. While the fund has routinely experienced up months of +25% or more, drawdowns of similar magnitude are also common. In 2022, during a challenging stretch of performance for Tech stocks, TECL experienced a -74% drawdown. For reference, QQQ ended 2022 down -33% for the year.

In light of what we view as nose-bleed-level valuations for the stocks in that TECL's exposure is concentrated, we think the fund could be poised for another period of challenging returns. While we certainly don't have a crystal ball, we think current valuations make it difficult to hold TECL for almost any period of time.

Designed for the adept investor with a strategy centered on short-term movements within the tech sector, TECL's leverage adds a layer of complexity and risk, especially at current levels.

Our pivotal concern is around the ETF's current valuation, with significant exposure to highly valued tech giants like Microsoft and Apple (which today trade near decade highs), we struggle to envision a path to further upside for the fund. The fund's concentrated exposure to high-flying tech stocks, compounded by its inherent volatility and 3x leverage, underscores what we believe is a significantly heightened downside risk for TECL.

As such, we are currently maintaining a Sell rating on TECL.