David Dee Delgado

David Dee Delgado

Today, we take a look at Delta Air Lines, Inc. (NYSE:DAL) which is a very cheap stock from a valuation basis compared to the overall market. It should be noted that airlines almost always trade at a deep discount to the overall market multiple (approximately 20 times earnings currently on the S&P 500), but Delta currently trades at just over seven times trailing earnings. The company made $6.25 a share in FY2023 on just over $54.6 billion in revenue. Delta had a rock-solid year in 2024 with pre-tax income nearly doubling to $5.2 billion, while return on investment capital rose approximately 500 bps to 13.4%.

The current analyst firm consensus has Delta making $6.46 a share in FY2024 and $7.51 a share in FY2025 on sales growth of four to five percent each year. The company had an operating free cash flow of $7.2 billion in FY2023, clear of Cap-Ex costs, Delta delivered $2 billion in free cash flow in FY2023. Delta's current market capitalization is approximately $29 billion.

Seeking Alpha

However, the stock has made a 50% move off its recent lows of late October and is quickly closing in on the highs the shares made this summer. The rally has seen some insiders take some chips off the table this quarter, with three insiders including the CEO selling just over $3.2 million collectively in February. Prior to that, a company director bought just over $630,000 worth of shares in October in the low $30s after the selloff over the last summer.

The company has also been impacted by the unfolding quality issues at The Boeing Company (BA) which I recently covered. Delta's CEO recently remarked that some plane deliveries could be pushed back out to 2027 in regard to the newest version of the 737 Max. Delta currently has orders in for one hundred 737 Max airliners with a list value of $13.5 billion, with options on another 30 aircraft. This risk is quite manageable, but could see negative news flow until Boeing makes substantial progress improving their production processes.

July 2023 Company Presentation

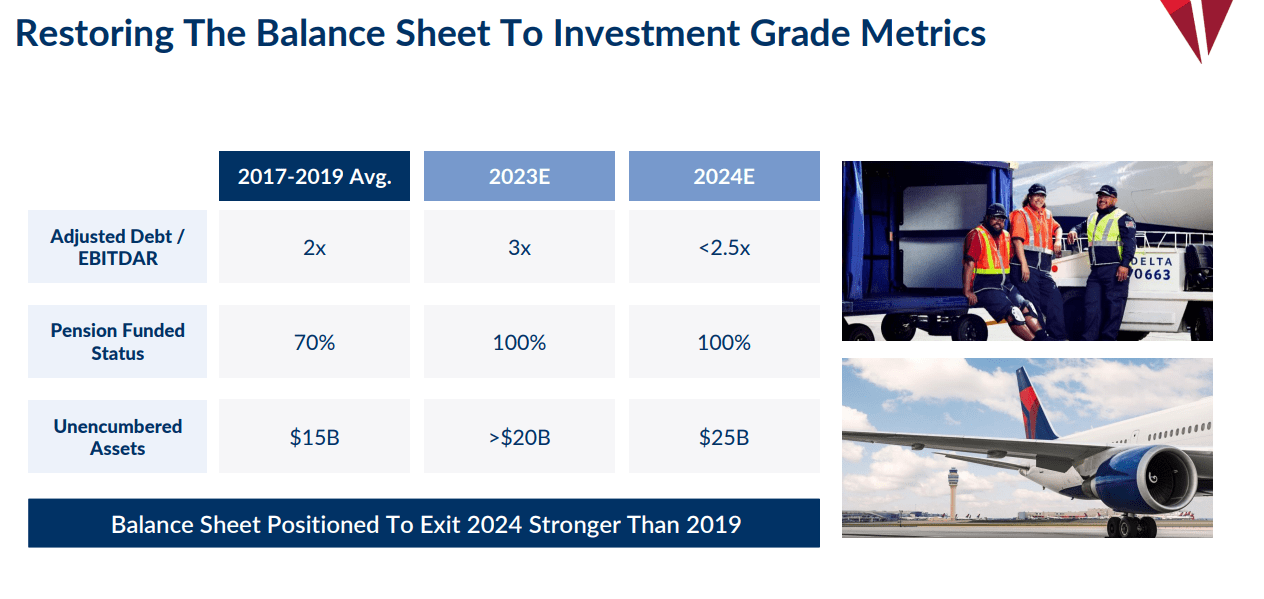

The company also faces a higher cost structure in the years ahead from a new four-year pilot union contract that was signed last year. The company has done a good job fully funding its pension plan over the past several years and leadership is committed to continuing to reduce balance sheet leverage. That said, Delta had $834 million of net interest expense in FY2023 even after paying off $4 billion in gross debt in 2023. Management has given initial FY2024 guidance calling for a free cash flow of between $3 billion to $4 billion during the fiscal year. This is after planned CapEx expenses of $5 billion. Leadership plans to pay down another $3 billion of 2024 debt maturities and also take ownership of 45 new airliners during the year. Delta also sees maintenance costs increasing by $350 million in FY2024.

2023 10-K

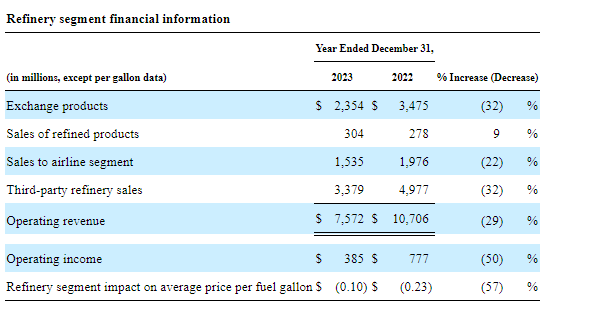

Crude oil prices (CL1:COM) have moved up significantly recently, meaning higher jet fuel costs to the industry. Delta Airline mitigates these costs somewhat by owning its own refinery operations, it should be noted.

2023 10-K

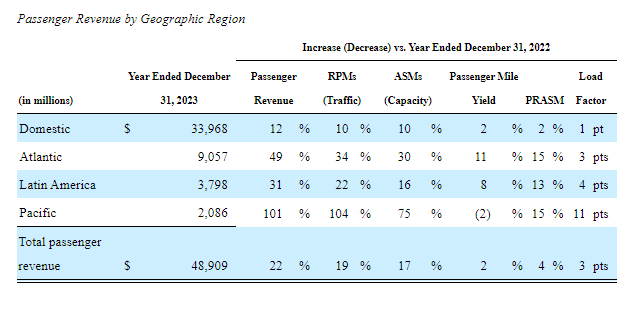

Delta Airlines is impacted greatly by the state of the U.S. economy where it gets approximately 70% of its overall revenue. That has been a positive over the past two quarters as U.S. GDP rang in the growth of 4.9% and 3.1% in the third and fourth quarters of 2023, respectively. However, GDP growth is predicted to slow in the coming quarters from those levels.

In addition, the economy faces several key risks that the market is content to ignore for now, as I highlighted in this article recently. If the country moves into a recession over the coming year, this is a scenario where airline stocks historically get hammered as demand slows especially for their highest margin market (business travelers).

Seeking Alpha

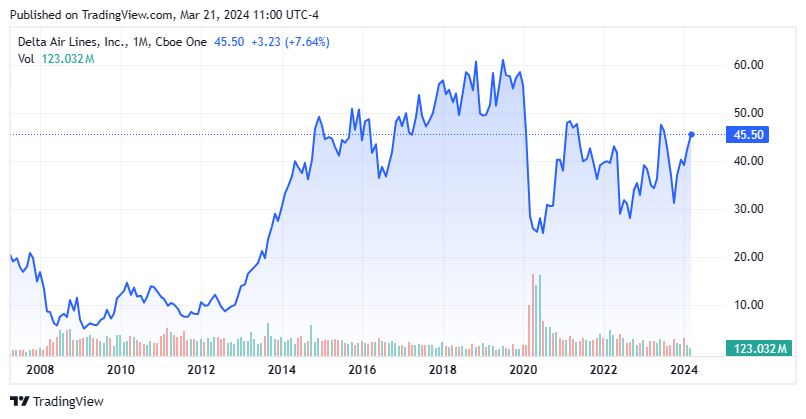

However, the number one reason I can't own Delta Airlines despite its cheap valuation and solid management, is that airline stocks are trading stocks not long-term holdings. Other names like American Airlines Group Inc. (AAL) are in the same boat, and AAL is even cheaper at under six times trailing earnings, it should be noted. As you can see from the chart above, the shares of Delta trade almost exactly where they did a decade ago and the equity also pays a paltry dividend (less than .7%).

The time you want to own Delta or any of the major airlines is after a significant negative event has cratered the stock. That has come in the past in the form of 09/11, the Great Financial Crisis, the Covid Lock Downs or even the brief Ebola scare of late 2014 that quickly took 25% to 30% off of major airline stocks before they rebounded sharply as that panic turned out to be short-lived.

In short, these are not instruments you want to chase after a 50% rise over the past five months despite Delta Air Lines, Inc. stock being cheap on a P/E and cash flow valuation basis and the company being well-managed overall.