Jeff Swensen

Jeff Swensen

Alcoa Corporation (NYSE:AA) produces and sells bauxite, alumina, and aluminum products worldwide. It mines bauxite, processes it into alumina, and smelts aluminum for various industries. Alcoa stands out as one of the largest international vertically integrated aluminum producers, with operations spread across 5 continents.

Statista

The company's primary raw material mining (bauxite) is located in Guinea and Australia, while refining occurs in the United States and Northern European countries. More than 50% of AA's revenue comes from the sale of primary aluminum, so as another Seeking Alpha contributor Invest Heroes noted previously, buying Alcoa stock represents a pure bet on aluminum price dynamics, as the fair value of the company's stocks fluctuates sharply in response to minor movements in raw material prices due to its high operational leverage.

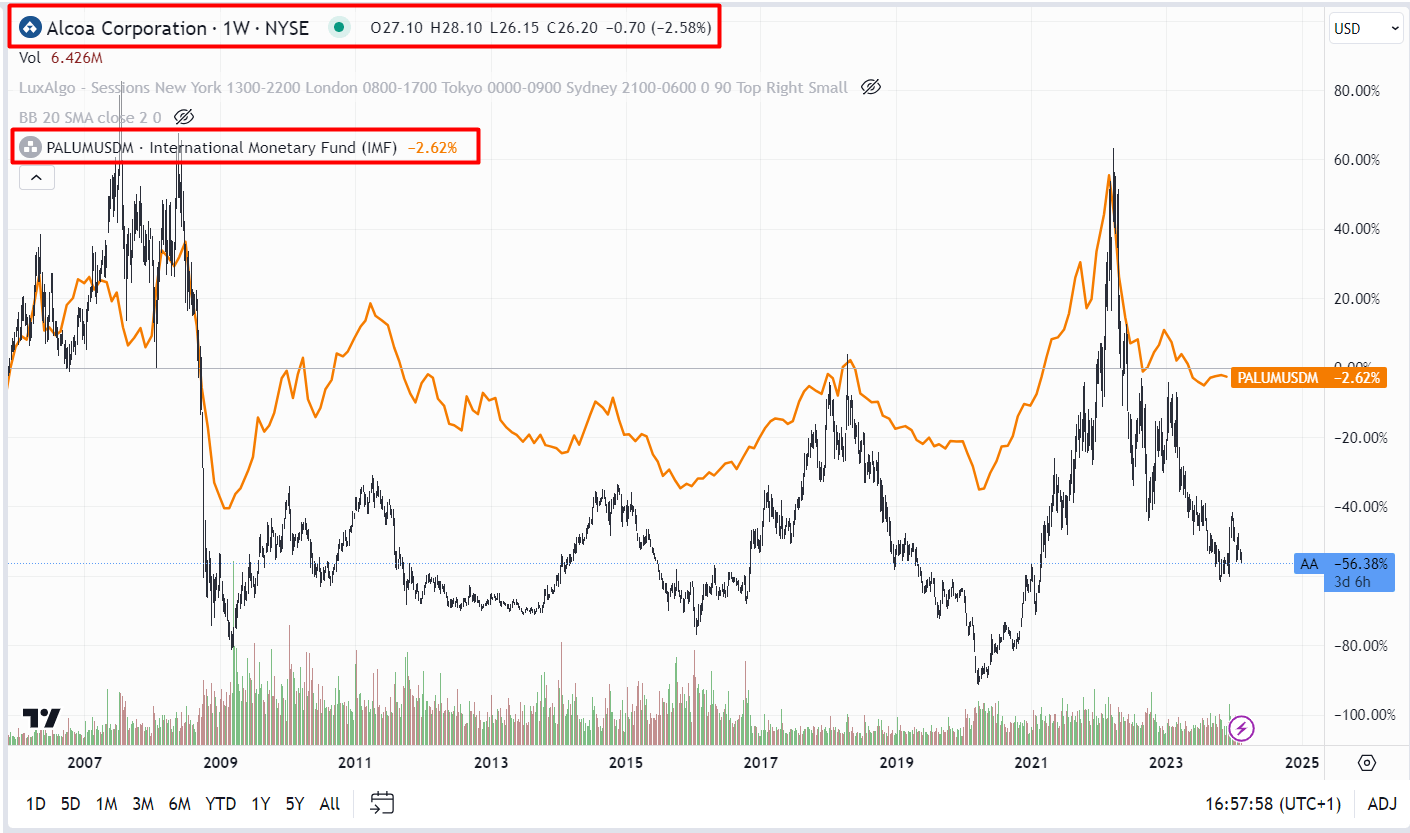

Over the past few years, the price of aluminum has decreased significantly, dropping by about 44.7% from its multi-year highs of $3,966/ton (February 2022) to ~$2,190/ton as of today, according to Tradingeconomics data. This decline has been attributed to a slowdown in global economic activity and reduced tension in the energy market. We can clearly see how this relationship has been reflected in the behavior of the AA stock in recent years (which once again confirms that AA moves as a derivative of the movement on the commodity):

TradingView.com, AA + aluminum prices since 2006

The main demand for aluminum is concentrated in the construction sector and transportation, accounting for 25% and 23% of consumption, respectively [DBS Group Research's data]. The remaining portions are almost evenly distributed among heavy industry (11%), the power sector (11%), foil and packaging production (9% and 8%), and others.

The data provided by Goldman Sachs in its February note (proprietary source) shows that the global aluminum market is quite heterogeneous today. In China, there was a deficit of ~1.1 million tons in the onshore primary aluminum market in 2023, which according to GS could widen to ~1.3 million tons this year and to ~2 million tons by FY2026. This massive deficit is currently offset by surpluses in the Western markets - and is likely to continue until the end of 2024:

![Goldman Sachs [February 2, 2024 - proprietary source]](https://static.seekingalpha.com/uploads/2024/2/27/49513514-1709025893650166_origin.png)

Goldman Sachs [February 2, 2024 - proprietary source]

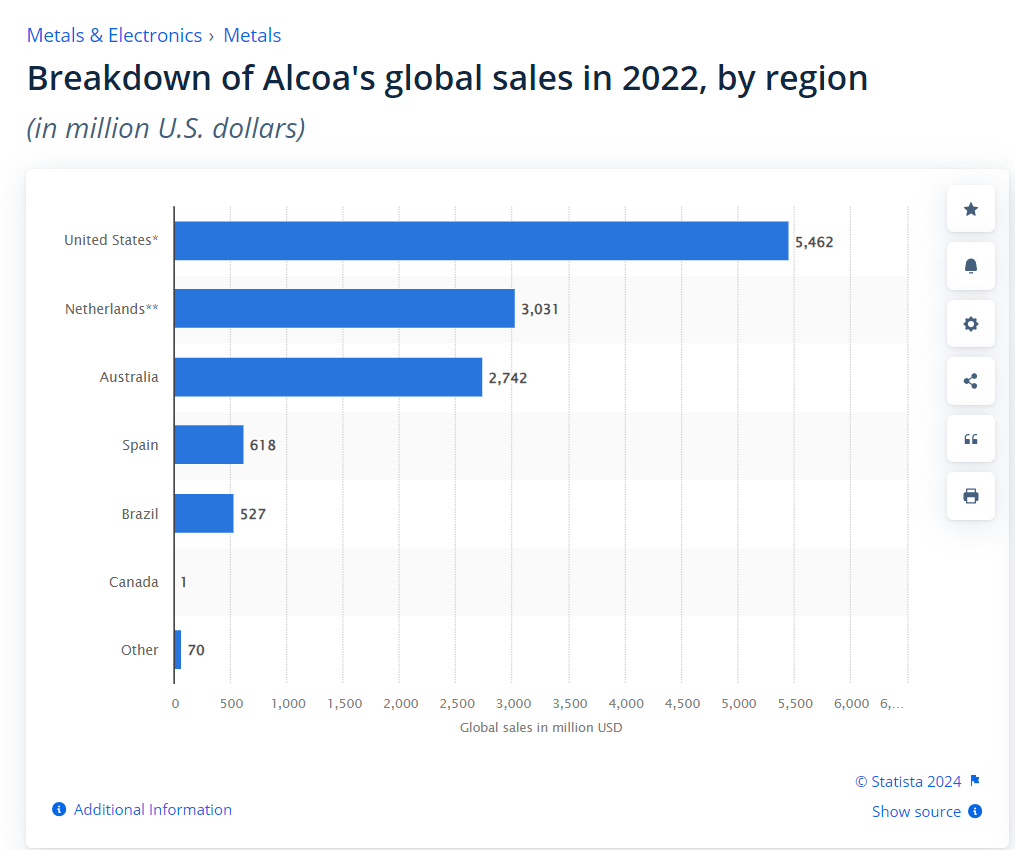

I already mentioned above that AA's most revenue comes from the sale of primary aluminum, but also important to note here - nothing of it comes from China, according to Statista data.

Statista

This means that aluminum sales take place in regions with a high risk of a manufacturing recession amid a surplus. Overall, demand for aluminum outside China fell by just under 2% in FY2023, with Europe being the biggest regional drag at -4%.

And the current feedback from both European and US physical markets points to a continuation of the sluggishness prevalent last year, GS notes.

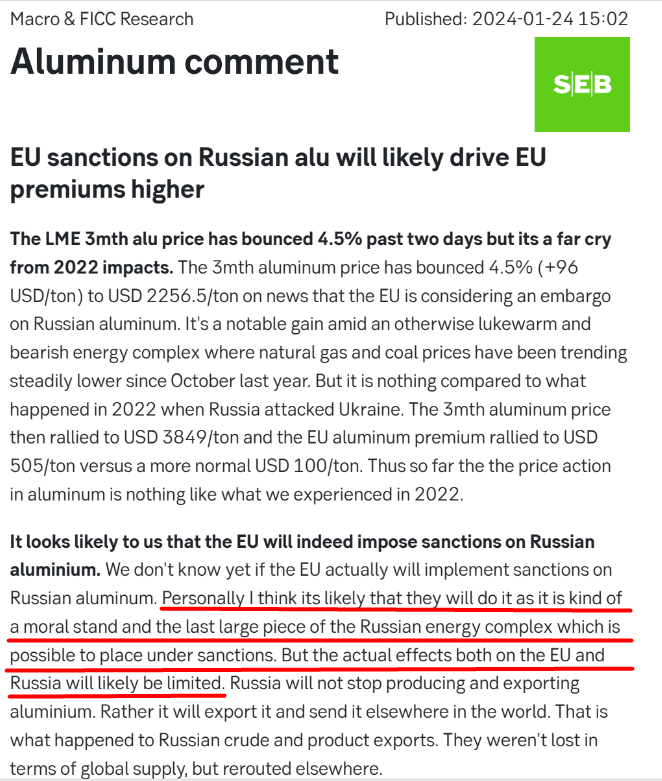

If you follow the political news, you have probably heard the news in recent days that the EU has adopted another package of sanctions against Russia, just in time for the anniversary of the invasion of Ukraine. Many experts assumed that the new package would also include restrictions on the sale of Russian aluminum to Europe.

SEB Group's report (January 2024, proprietary source), the author's notes

After the start of the war in Eastern Europe, Alcoa repeatedly tried for sanctions against Russian aluminum - this is understandable because, from an economic point of view, such a ban on Russian raw materials import would immediately make Alcoa many times stronger on the world stage.

Reuters

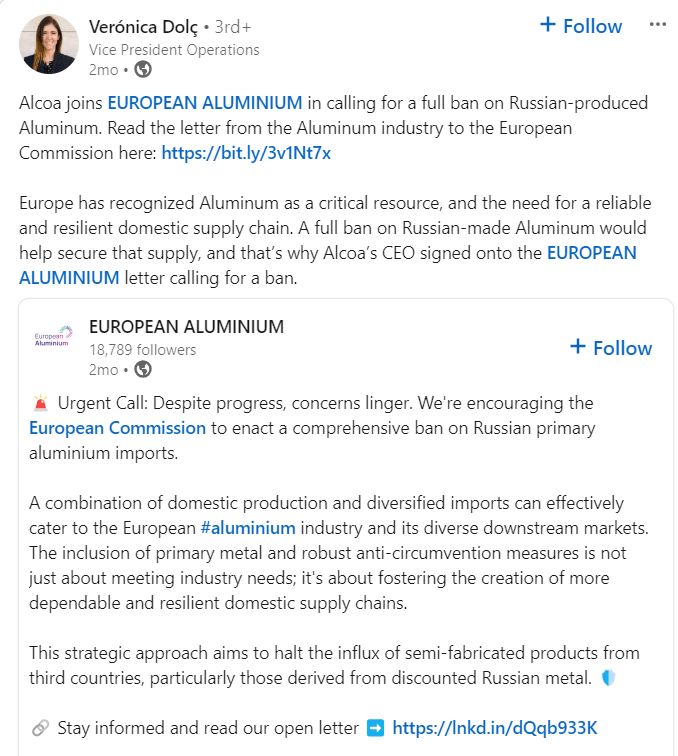

And in addition to influencing the US, Alcoa also tried to support its interests in Europe as I see it based on Verónica Dolç's recent post on LinkedIn (she is Alcoa's Vice President and simultaneously a Board Member of the European Aluminum Association):

But I think such a ban would likely significantly impact production in Europe and force Europeans to pay a premium for non-Russian aluminum. Therefore, Alcoa could be the main beneficiary of such a scenario.

In my opinion, such a decision would lead to even more serious negative consequences for Europe: Prices would begin to rise against a backdrop of already weak demand, greatly increasing the risk of a recession in production in the region. Five European industry associations agree with me, according to Euronews:

In a joint statement, the associations said they sent a letter to EU authorities and "requested the urgent intervention of the European Commission and of EU member states against threats of bans, high tariffs or sanctions on Russian aluminium which represent an imminent and vital threat to the European aluminium industry."

The statement said those boycotting or calling for measures against Russian metal "are either its main competitors or they enjoy supply options that are not available to the vast majority of the European aluminium value-chain."

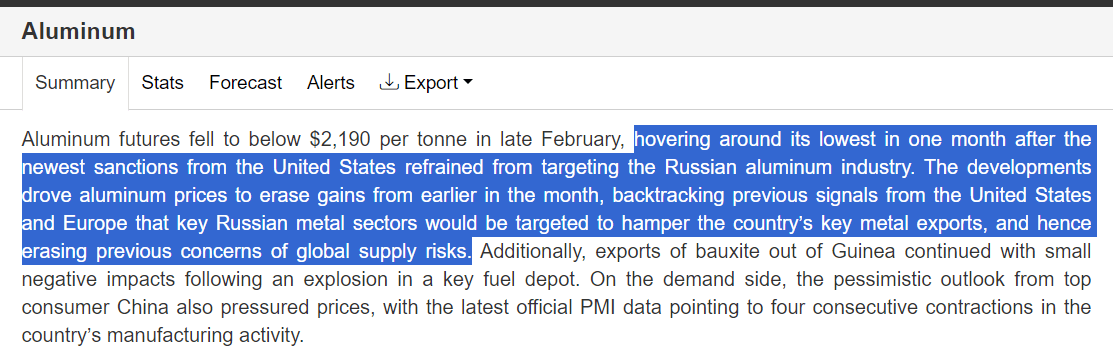

But eventually, the boycott did not happen - Europeans defended the right to more affordable raw materials, and therefore global aluminum prices did not rise, but even corrected slightly, giving back a significant part of the previous gain:

TradingEconomics.com

This removes the potential bullish catalyst for Alcoa to get part of the EU market at better prices. At least for now. So considering the data from GS on the projected surplus in the EU, which will remain until the end of 2024, the whole backdrop cannot be described as favorable for AA, in my view.

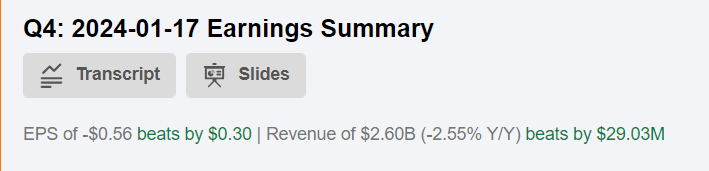

Let's now touch on the company's financial performance. In Q4 FY2023, Alcoa's adjusted EBITDA saw a significant uptick, climbing by 30% to $172 million. Despite losses, Alcoa's EBITDA comfortably covers interest expenses by a factor of 7.

The firm reported an adjusted net loss of -$0.56 that surpassed market expectations, with revenue holding steady at $2.6 billion compared to the previous quarter (also beat the consensus).

Seeking Alpha, AA

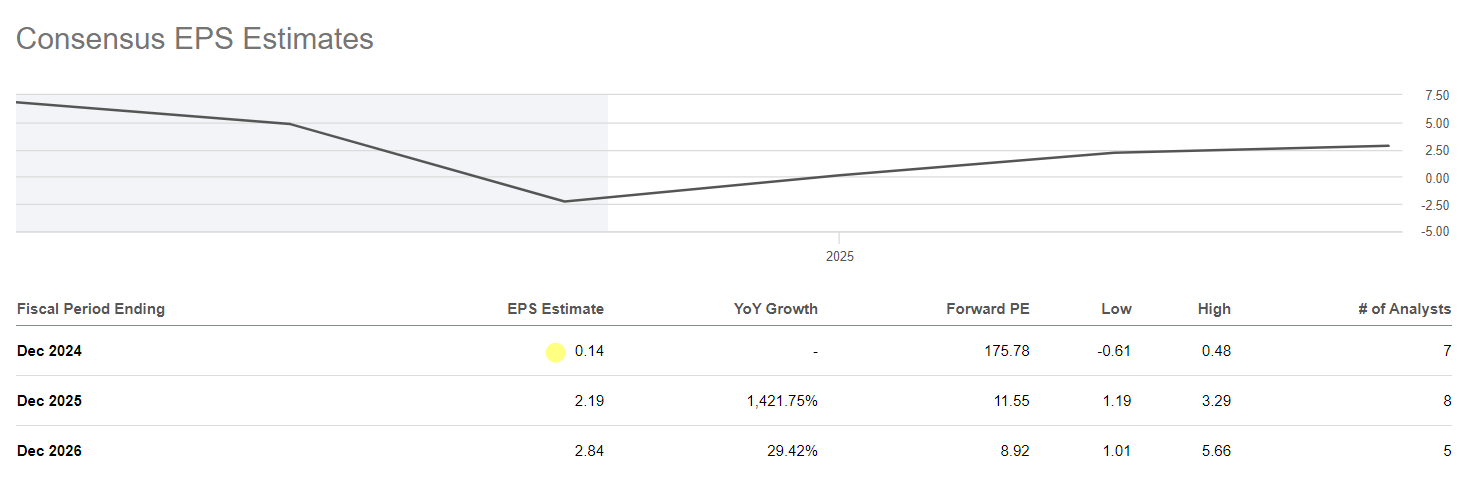

One strikingly positive conclusion from this data is the reduction in the company's net loss by a factor of 2.6 compared to the previous year. But we have AA's guidance on hand: the company expects alumina shipments of 12.7-12.9 million tons, which corresponds to the volume of ~12.8 million tons in FY2023 but is below the volume of ~13.1 million tons in FY2022 (Argus Research, proprietary source). In the aluminum segment, the company expects sales of 2.5-2.6 million tons, consistent with FY2023 and FY2022. This means that if we assume that prices remain depressed until the end of 2024, the company may report a net loss at such volumes again. And this goes against what the Wall Street consensus expects from Alcoa today:

Seeking Alpha, AA, author's notes

In terms of the company's valuation, Alcoa's P/E ratios vary quite widely in a highly cyclical industry: a comparison of the implied ratios for 2024 and 2025 shows this. Assuming that EPS estimates are indeed slightly overestimated today based on recent news (and with the resulting impact on AA's earnings), the P/E ratio for the 2025 financial year could even be a couple of times higher than today's 11.55x. So to account for this risk, the stock needs to fall even lower, in my view.

Given the cyclical nature of Alcoa, I would not risk giving clear stock price targets here because everything can change overnight. What I can give, however, is an assessment of the situation surrounding Alcoa: the bullish catalyst in the form of sanctions against Russian aluminum has not materialized, the ex-China market will likely be in surplus by the end of 2024, and manufacturing activity in the company's key end markets has not yet improved, judging by recent data. At the same time, Wall Street is forecasting that Alcoa's EPS will rise to a positive figure in FY2024. Yes, this forecast is influenced by a number of factors. The company is doing quite a bit in terms of cost management, for example. But I don't see how the situation can change dramatically for AA at current commodity prices in the foreseeable future.

I would like to reconsider my 'Hold' rating by the end of the year. But for now, I think buying Alcoa stock is too risky.

Thanks for reading!