nicolas_

nicolas_

Revvity, Inc (NYSE:RVTY), formerly known as PerkinElmer, is a major laboratory instrument and service provider to the healthcare industry. According to data from instrument platform manufacturers such as Tecan Group (OTCPK:TCHBF), Revvity is a provider of niche assay specialties such as DELFIA, Alpha38, and BRET2, along with high end analytical equipment. Also, the company remains the primary choice for prenatal and newborn screening, with the newborn heel prick remaining the industry choice (70% market share and state mandated procedure). Across the entire product portfolio, Revvity has generated enough superiority to earn a “narrow moat” rating from Morningstar.

Advanced tools and techniques have done well to increase profitability for the company as they differentiate themselves from other diversified peers. The issue is that peers have invested heavily in inorganic growth opportunities, preventing RVTY shares from gaining traction. Why choose PerkinElmer in the past when TMO was growing revenues more than twice as fast. Now that the market is cooling off, but internal financial improvements are well underway, I believe a new phase is beginning for the company. As such, I expect that there is an opportunity for Revvity to outperform in the intermediate term.

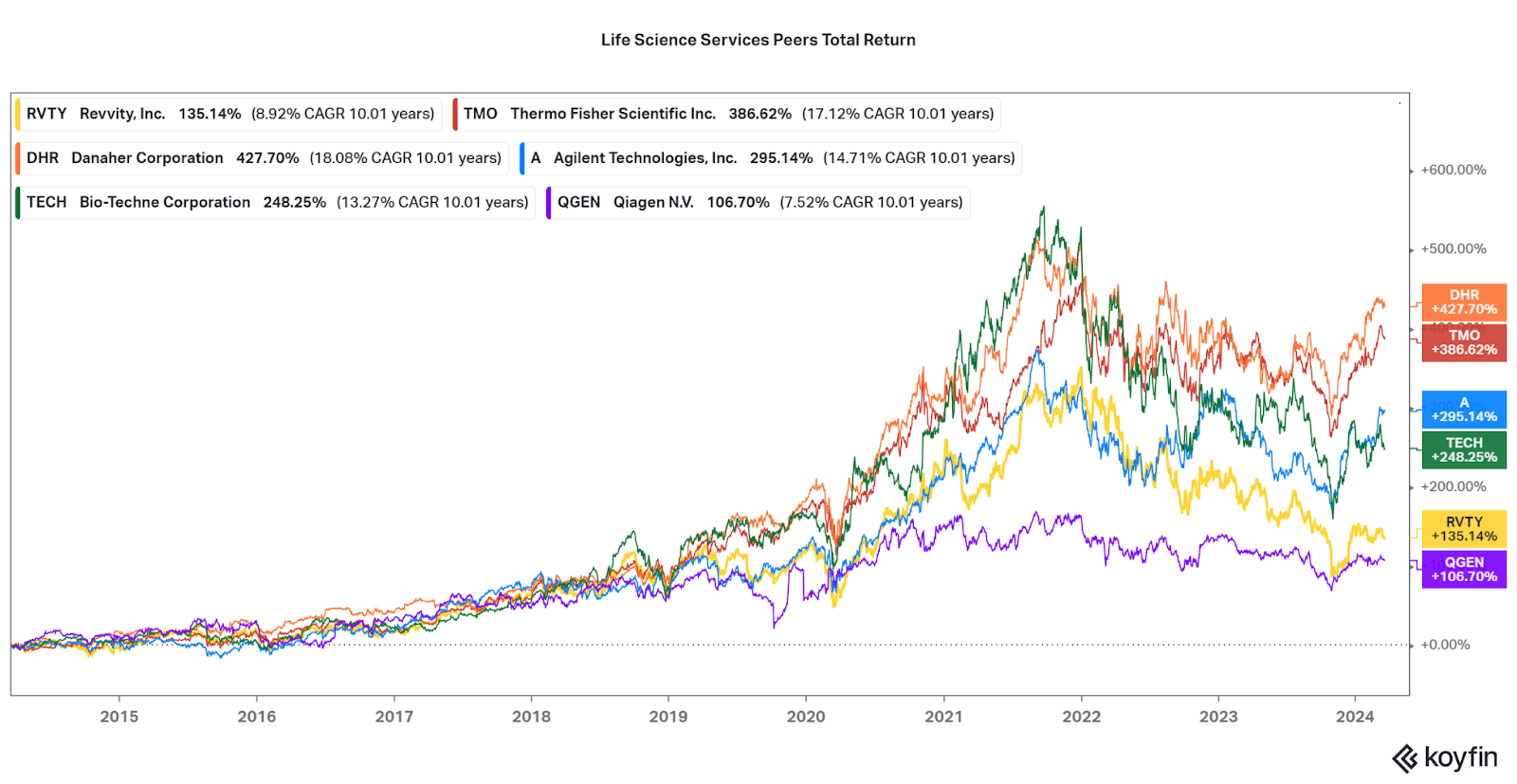

Over the past 20 years, Revvity has returned 10.5% per year for investors, above the 9.85% of the market benchmark Vanguard 500 Index. Returns may be market-beating, but are below close industry peers such as Thermo Fisher (TMO) at 17%, Danaher (DHR) at 15%, and even Agilent (A) at 10.7%. The discrepancy can primarily be attributed to underperformance, particularly in regards to profit generation and growth. If Revvity continues on a weak path, they may end up performing like profitable, but slow moving Qiagen (QGEN). However, if the recent business restructuring is a signal of things to come, I expect shares will perform closer to the giants, or growth oriented peers such as Bio-Techne (TECH), which has returned 11.6% annually.

A backtest of total returns for six Life Sciences Services peers over the past 20 years. (Portfolio Visualizer)

10 Year Returns Chart (Koyfin)

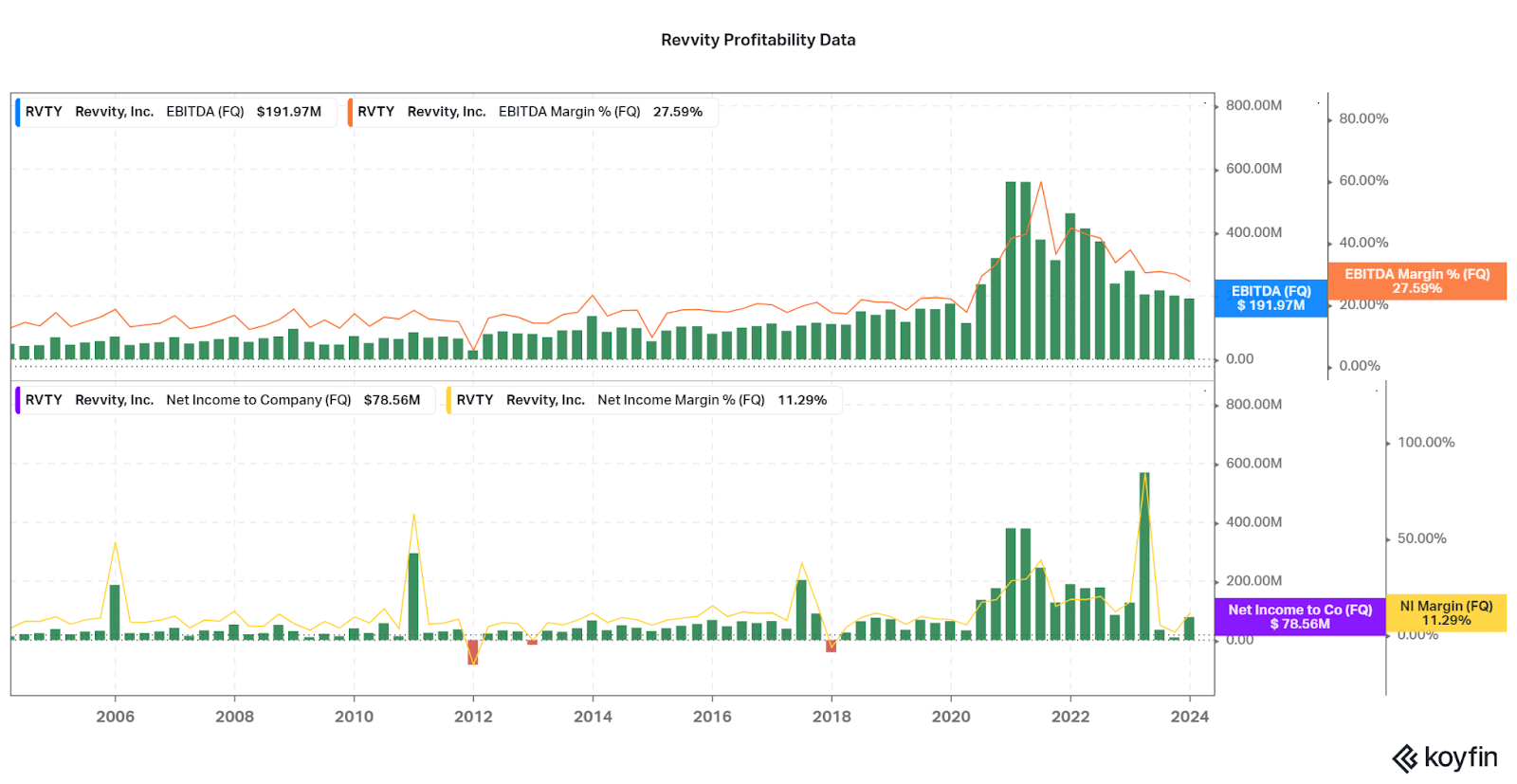

In order to improve the internal business structure, Revvity has copied larger peer Danaher by spinning off their applied/non-healthcare sciences unit to private equity. This is to increase operating margins by focusing on life science and diagnostic consumables. This has driven recurring revenue up for RVTY, allowing operating and net income margins to reach all-time highs. However, a lack of diversification continues to cause margin cyclicality, and so it will also be necessary for Revvity to take the inorganic growth path that is familiar with TMO and DHR.

Management has already announced their intention to pursue this course, and a few high quality M&A can go a long way in this environment with valuations down. As an example, I recently discussed Cytek Biosciences (CTKB) as a leading instrument developer looking to expand into reagent recurring sales, and there may be synergies between the two firms. This will also help drive diversification away from less growth oriented diagnostics markets, such as prenatal screening, and into biotech research. As I highlight below, the Life Sciences segment is far more valuable than diagnostics.

Koyfin

While Revvity’s EBITDA/Operating Margins are in line with peers as recurring revenues reach 80% of sales, net income weakness makes the firm expensive on a trailing PE basis. However, with a current EV/EBITDA of 18x, lower than all peers aside from Qiagen, there is opportunity for investors. It is important that margins do improve as the bear market ends, but the low valuation following a 40%+ decline in share price from recent highs allows for downside protection. While rates have not come down yet, equilibrium may be found and reignite biotech and diagnostic research spending in the intermediate-term. I believe that shares are close to bottoming when considering the potential for significant inorganic growth.

Although, I will note that the balance sheet is now the biggest financial hindrance and risk-point moving forward when compared to peers. The many years of restructuring have not led to a sub 1.5x leverage ratio, unlike most peers, and so a larger sized acquisition may be off the table. Or, RVTY will initiate a leveraged growth phase similar to Thermo Fisher, but the management team may be unequipped to handle that burden. The BioLegend acquisition has certainly ended up being costly. Therefore, I hope to see leverage fall below 2.0x at the next earnings release before a major announcement occurs, and if one does happen, for leverage to remain below 4.0x (particularly since TTM EBITDA generation has been relatively strong).

The other important insight that comparative analysis points out is that Life Sciences remain superior to Diagnostics. With Revvity seeing closer to a 40/60 mix of LS/DX sales, the historically lower profit margins have their primary cause. While DX stalwart Qiagen does offer significant profitability, the growth rate issue also stands out from an organic standpoint, although recent EPS growth has upset that pattern (although attributed to a comedown from pandemic era success). I prefer that Revvity focuses on the Life Sciences for future growth, akin to Bio-Techne, albeit while maintaining their market presence in the diagnostic niches they own.

Company | Recurring Revenues Mix 2023 | Operating Margin (% by Life Sciences / Diagnostics) | 10 Year EPS CAGR (%) | Current/ 5 Year Avg. NI Margin (%) | Leverage (Net Debt / EBITDA) | P/E | EV / EBITDA |

Revvity | 80 | 37/21 | 14 | 25/17 | 2.4 | 72 | 18 |

Thermo Fisher | 82 | 36/22 (Adj) | 16 | 14/16 | 3.1 | 38 | 22 |

Danaher (Life Sciences) | 75-80 | 19/26 | 5.3 | 20/19 | 1.4 | 44 | 26 |

Agilent | 60 | 29/21 | 6.8 | 18/18 | 0.9 | 35 | 26 |

Qiagen (DX-focus) | >80 | 27 (Adj) | 17 | 17/16 | 1.0 | 29 | 16 |

Bio-techne (LS-focus) | 90 | 30 (T6M Adj) | 6.1 | 20/23 | 0.7 | 51 | 34 |

Table 1. Source: Compiled by Author. Seeking Alpha, Koyfin, and company data.

Despite some interest rate headwinds hindering spending in the pre-revenue healthcare space, Revvity does have catalysts in place to drive outperformance moving forward. In particular, I do believe management’s business restructuring is net-positive, particularly if inorganic investments in areas of high margins continue to drive differentiation from peers. At current prices, Morningstar agrees with my sentiment, providing a five-star rating to RVTY. And, if growth remains at historical levels, the data shows that the company still outperforms the broader market in the long-term (a benefit of the strong healthcare industry).

I do not think there is a need to bottom fish, or try to time the best buy point, but I expect recurring investments over the next few months to end up fruitful for investors. We already see some players in the sector picking up momentum, such as Bruker (BRKR) surpassing all-time highs, while Revvity remains suppressed. With a proper maturation, I believe RVTY will outperform the listed peers and market. I look forward to seeing how Revvity matures.

Thanks for reading. Feel free to share your thoughts below.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.